Natural Gas Markets

LNG Exports To Boost Dry Gas Drilling, Underscore America’s Resource Vitality

By Javier Díaz

DENVER–The winter of 2013-14 served as an abrupt reminder that natural gas prices are highly sensitive to weather fluctuations, reducing mid-February storage volumes to their lowest seasonal levels in a decade and pushing NYMEX prices to $7-$8 an MMBtu. While U.S. liquefied natural gas exports will not impact the market anywhere nearly as dramatically as weather, they do have the potential to consistently help maintain prices at levels sufficient to bolster dry gas activity and increase domestic supply availability.

The strengthening of prices from LNG exports is expected to start in 2016, as export terminals come on line and add trains to reach their planned capacities. Average annual prices will surpass $5 an MMBtu in absolute terms by 2022. After adjusting for inflation, they likely will average around $5/MMBtu at least until 2035, with occasional price fluctuations that LNG will serve to temper.

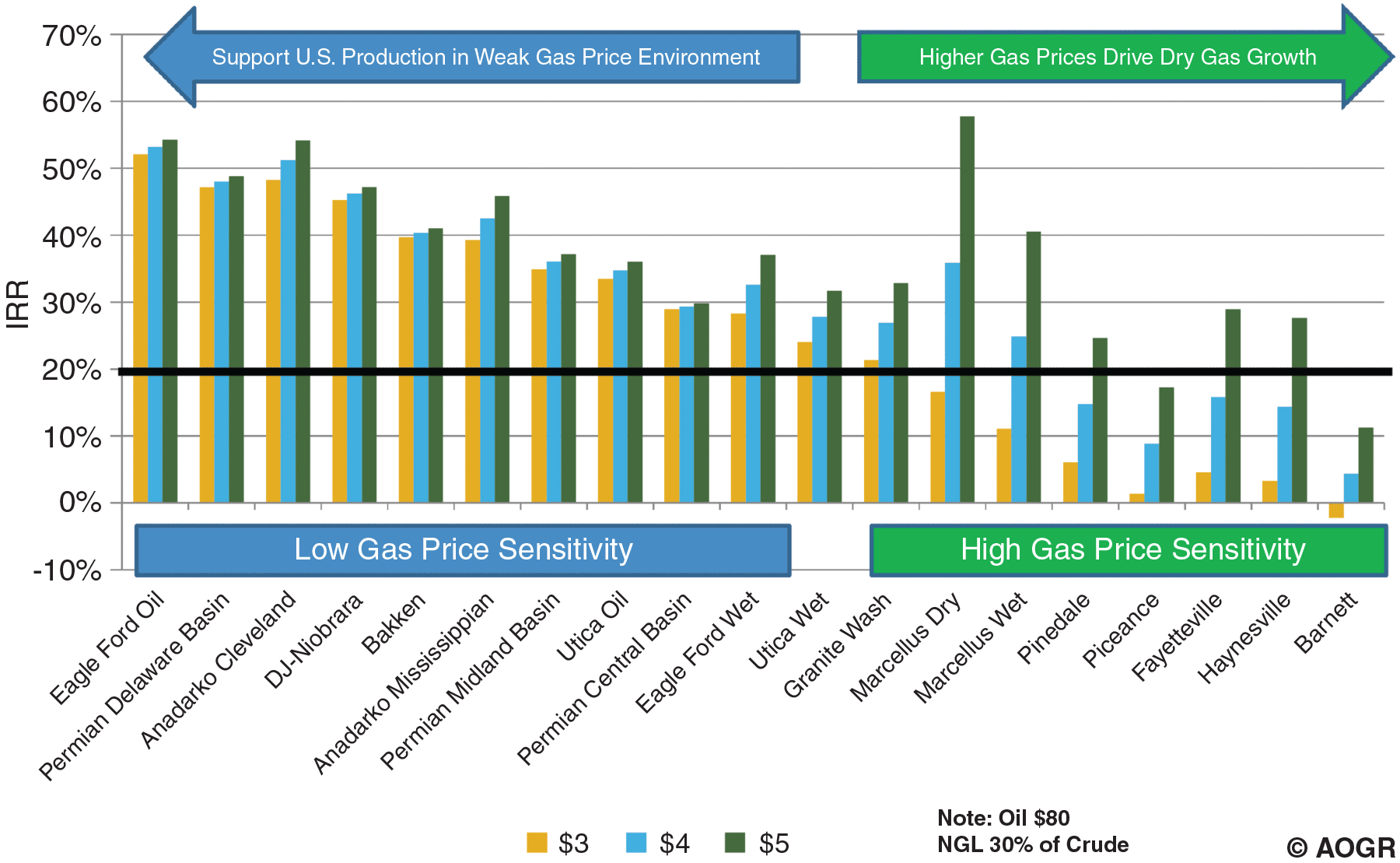

The modest price increase will have a limited effect on the economics of oil and wet gas plays, but it will increase significantly the profitability of dry gas shale plays such as the Fayetteville, Haynesville and parts of the Marcellus. By 2018, rates of return in these plays should exceed 20 percent, enough to justify additional drilling (Figure 1).

FIGURE 1

Play IRRs at Various Gas Prices

These predictions reflect the growing demand for LNG. Between 2013 and 2020, global demand should increase 15.4 billion cubic feet a day in response to rising energy consumption, particularly in Asia, and an environmentally motivated desire to use natural gas rather than coal or oil.

The most significant demand increases should occur in China. That is attributable not only to its growing economy and energy consumption, but also to its continuing efforts to reduce air pollution in many of its cities by cutting coal consumption, including switching power generation capacity from coal to clean-burning natural gas.

China has made great strides toward developing its potentially vast unconventional reserves, but it does not have the infrastructure to get production where it needs to go. So at least in the short and medium terms, it will be more economical for China to build import terminals near its populated areas and industrial centers.

Demand Limiters

Two factors could limit LNG demand. The first is changing policies on nuclear power production, particularly in Japan, the world’s largest LNG importer with one-third of the market. BENTEK Energy expects Japan to restart some of the nuclear power plants that have been off line since the 2011 earthquake, but if the plants remain idle, demand could rise an additional 2.0 Bcf/d-2.5 Bcf/d by 2020.

Because it is the second largest market for LNG, South Korea’s philosophy toward nuclear power also will greatly influence demand. Like Japan, the republic has long embraced nuclear power as a source of affordable, carbon-free energy. However, the public’s trust in nuclear power has declined in the wake of the 2011 earthquake’s disastrous impact on the Fukushima plant in Japan, and the discovery last year that the safety certificates for components at several South Korean plants had been forged.

Perhaps as a result, the country’s latest long-term plan aims for nuclear power to account for 29 percent of its energy mix by 2035. While this still will require additional nuclear power plants, it is a substantial decrease relative to the previous plan, which had nuclear power providing 41 percent in 2030.

In other areas, including the growing markets in India and China, price liberalization could reduce LNG demand significantly. For example, in India, the government-made price formula may double gas prices by mid-2014. That would encourage domestic production, thereby reducing demand for LNG temporarily, though in the long run Indian demand is expected to continue growing.

Other demand limiters would be potential future Russian pipeline supply into China, and future shale gas developments around the world. Despite these potential limiters, we see demand continuing to grow. For U.S. natural gas producers, that is good news, for the United States is likely to secure a significant share of the total global LNG market.

U.S. Advantages

As of late March, the U.S. Department of Energy had received applications requesting permission to export 38.51 Bcf/d from the continental United States. While only a few of the projects behind these applications will be approved, funded and built, it is no surprise so many have been proposed, given the numerous advantages the United States has over other countries seeking to export LNG.

With abundant natural gas supply available, the biggest advantage is that U.S. LNG prices will be linked to natural gas, not crude oil. That could make a huge difference for Japan and other importers in the Asia-Pacific region, where most LNG contracts set the price at 14.85 percent of the Japanese crude cocktail, the average price the country pays for its oil imports. U.S. LNG imports will provide Asian buyers an option to diversify their LNG sources and reduce their costs.

The United States also has well-developed midstream infrastructure. Unlike the vast majority of export terminals proposed elsewhere, whose backers must not only build a terminal but also develop a field to supply it, U.S. projects need only connect to the pipeline network to access a diverse, reliable and cost-efficient supply.

The United States’ third advantage is access to labor. Like their international counterparts, U.S.-based developers must draw from the small pool of workers with the skill sets required to build LNG terminals. However, it is much easier to get people to the United States than it is to send them to the remote locations where many international projects have been proposed.

These advantages make it much easier for U.S. projects to secure the long-term, take-or-pay contracts they need to mitigate the risk associated with building LNG terminals, attract funding, and justify final investment approval.

Two years ago, securing such contracts was difficult even in the United States because of regulatory uncertainty. Liquefaction terminals must receive a permit from DOE to export LNG to countries with which the United States does not have a free trade agreement (FTA). Those countries include most of the target markets in Asia, such as Japan and China, with South Korea being the most remarkable exception.

DOE took two years to approve the first permit and another year to approve the second, so potential buyers were understandably worried that proposed terminals would never clear the necessary regulatory hurdles to become a reality.

Today, however, with six terminals approved, DOE has established a reassuring track record of approving applications only a few months apart. As a result, all the U.S. projects that involve converting an unused LNG import terminal into an export terminal have been able to secure contracts for most of their proposed capacities.

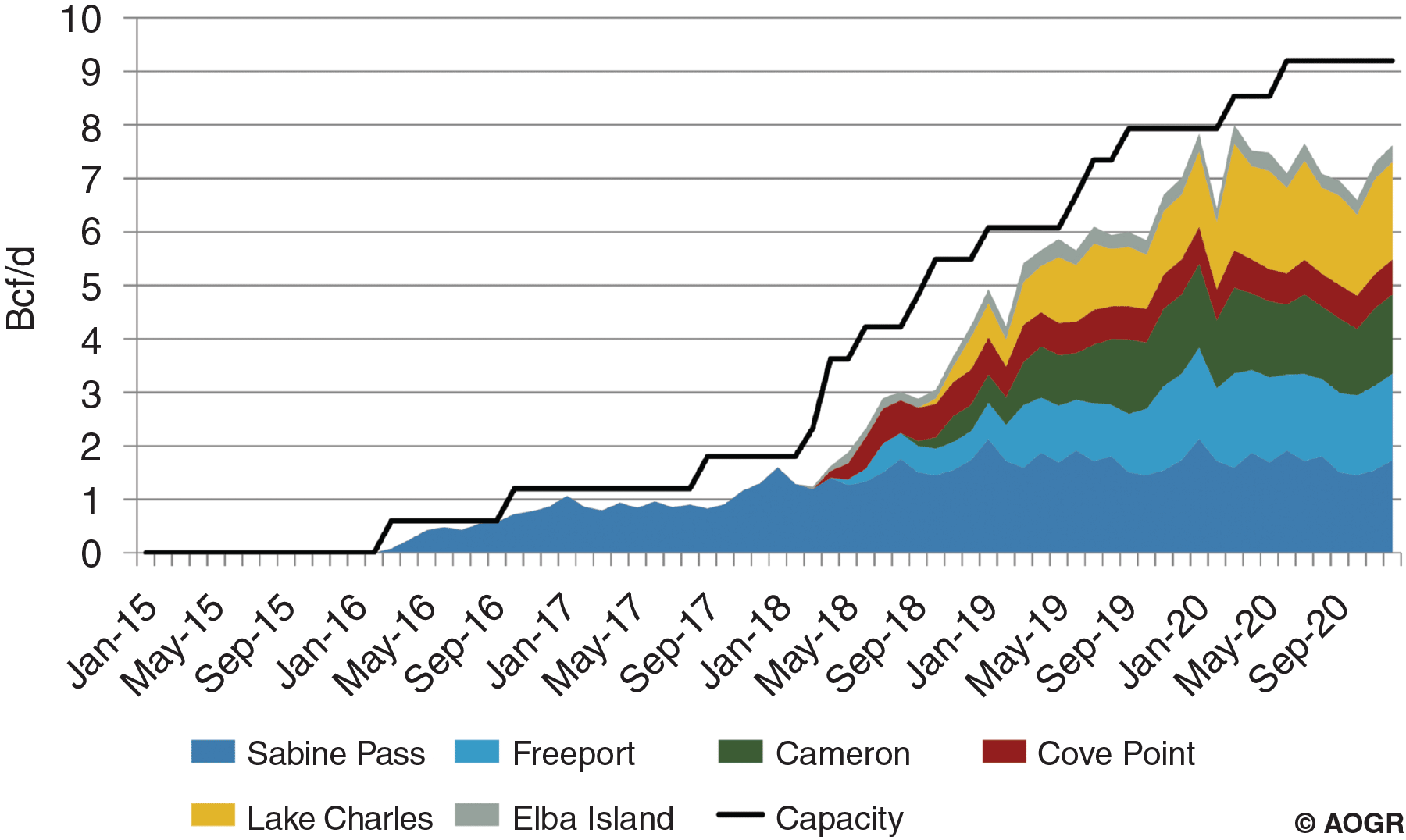

Conservative Forecast

The United States has eight LNG import terminals that plan to convert to LNG export facilities. BENTEK’s intentionally conservative base forecast assumes that six of these terminal conversions will be completed:

- Cheniere Energy’s Sabine Pass in Cameron Parish, La., which has DOE’s approval to export 2.2 billion cubic feet of gas a day to non-FTA countries;

- Freeport LNG’s terminal in Freeport, Tx., which is permitted to export 1.8 Bcf/d to non-FTA countries;

- Energy Transfer Partners’ terminal in Lake Charles, La., which has approval to export 2.0 Bcf/d;

- Sempra LNG’s Cameron terminal in Hackberry, La., which has approval to export 1.70 Bcf/d;

- Dominion’s Cove Point facility in Calvert County, Md., which has approval to export 770 million cubic feet a day to non-FTA countries; and

- Kinder Morgan’s Southern LNG terminal on Elba Island near Savannah, Ga., which seeks approval to export 500 MMcf/d to non-FTA countries.

Since five of these facilities have permits to export to non-FTA countries and all six have contracts, this base case is extremely conservative. However, there is still some risk, for with the exception of Sabine Pass, the companies still need approval from the Federal Energy Regulatory Commission to construct and operate the necessary facilities. Assuming all six obtain that approval, we expect U.S. exports to average 7.3 Bcf/d by 2020 (Figure 2).

FIGURE 2

Conservative U.S. LNG Export Forecast

That would give the United States a vital role in the global LNG market, which we expect to be undersupplied throughout the rest of the decade. If delays keep competing projects in Canada, Russia, Australia and East Africa from coming on line, the United States could become the pivotal player in terms of bringing global LNG supply and demand in balance.

That may well happen, as delays and cost overruns have become the norm in international LNG export terminal development. Consider Australia’s experience with green-field LNG infrastructure projects. The cost estimate for the Gorgon project has risen from $37 billion in 2009 to $54 billion in 2013, and continues to grow. Even the much simpler Pluto project, the last Australian terminal to finish construction, came on line a year late and $2.7 billion over budget.

These delays occur because the projects are in remote areas that require investing in and developing production, pipelines, and ports in addition to terminals. Similar delays have been seen in Angola and are expected in Canada and East Africa.

In other cases, projects have had trouble securing contracts because the developers want to maintain oil-based prices, which potential buyers generally oppose, given the likely availability of gas-linked supplies from the United States.

The United States has no shortage of projects that could fill the gap created by delays and cancellations elsewhere. In addition to the two import terminal conversions excluded from the base forecast–Kinder Morgan’s Gulf LNG terminal in Pascagoula, Ms., and the ExxonMobil and Qatar Petroleum International-backed terminal in Sabine Pass, Tx.–several green-field projects could prove viable.

These include Magnolia in Lake Charles, La., Cheniere’s terminal in Corpus Christi, Tx., the Excelerate floating export project in Lavaca Bay, and the Jordan Cove project in Oregon. Jordan Cove has been permitted by DOE to export LNG to non-FTA countries and has approval from Canada’s National Energy Board to export Canadian gas.

Together, these six projects’ capacity exceeds 8 Bcf/d. Should LNG projects in Australia, East Africa, Russia and Canada experience delays or cancellations, this additional capacity will enable the United States to fill the void in the global LNG market. This possibility would have an appreciable effect on U.S. demand and natural gas fundamentals.

Requirements

For the United States’ export dreams to become a reality, the market will need to supply an obvious, but often overlooked requirement: ships capable of carrying LNG long distances to premium markets in Asia. Our conservative base-case scenario will require 112 ships. Estimates indicate that there should be enough shipyard capacity to build them. They have yet to be ordered, but we expect they ultimately will get built and be placed into service.

Would-be importers will need to account for the difference in heat content between U.S. natural gas specifications and higher requirements from other markets, such as Japan, South Korea and Taiwan. Power generators could accomplish this by adjusting turbines, pipelines and storage facilities to accommodate lean gas, a step already being taken by Tokyo Electric Power and other key companies. Importers that serve residential and industrial customers and have higher heating value requirements will need to spike U.S. LNG with LPGs to keep it from damaging their customers’ equipment.

In the United States, LNG exports should have a modest effect on domestic gas prices, with a resulting minimal impact on energy costs for the residential sector as well as large industrial and power consumers. While the bolstered price will be sufficient to spur activity in dry gas shale plays, domestic manufacturers should continue to maintain an energy cost advantage over global competitors. As a result, the jobs, revenue, and trade created by exports are expected to yield a net benefit to the U.S. economy, in line with DOE conclusions.

JAVIER DÍAZ heads LNG analytics for BENTEK Energy, a unit of Platts, where he has developed a full suite of LNG products and analytical tools for predicting LNG transportation and production costs, supply and demand, and prices. He also has authored reports that cover the Atlantic and Pacific basins, global markets and North American LNG exports, as well as the BENTEK content included in Platts’ “LNG Daily.” Previously, Díaz served as the chief operating officer of the 8th Continent Project, which received the 2009 Jefferson Economic Council’s Genesis Award, “Economic Developer of the Year,” for creating jobs, investment opportunities and economic expansion within Jefferson County, Co. He also held a research faculty position at the Colorado School of Mines’ Center for Space Resources.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.