LNG and Data Center Demand, International Wildcards Top 2025 Demand Drivers

By Dennis Kissler and Cristina Stellar

TULSA–Price volatility is an inherent part of the business of oil and gas. Over the past four years, West Texas Intermediate crude oil closed as low as $52.00 a barrel and as high as $114.84, but averaged in the $70s-$80s through most of 2024. Natural gas spot prices on the Henry Hub ranged from $1.49 to $8.81, and floundered through much of 2024 at historical lows.

Understandably, as the energy industry looks to 2025, the prevailing question is: “What will happen to oil and gas prices?” The answer is, of course, it depends. As usual, there are many wildcards in both sectors. Nevertheless, there are some prevailing trends that can yield some directional insights into where prices are going.

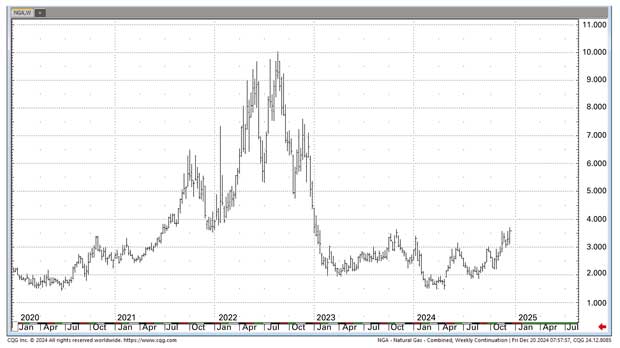

Let’s start with natural gas. Coming into 2025, natural gas supplies remain ample. Although electricity demand was up during the summer, it still fell short of pulling hefty natural gas supplies down. Meanwhile, the hurricane season during the fourth quarter damaged natural gas demand more than it constrained supplies, especially in the case of Hurricane Milton. Simply put, storage will need to contract substantially in what remains of winter 2024-25 to give a significant lift to prices.

Long-Term Drivers

Waha basis prices in Texas have weighed down prices (Figure 1). However, that should be improving with added pipeline takeaway capacity, such as through the Matterhorn Express Pipeline and increased exports flowing into Mexico.

Liquefied natural gas takeaway is the longer-term bullish driver. LNG export capacity is expected to reach all-time highs and should alleviate excess natural gas storage and additional production, but it will do little to prices in 2025 if we see mild weather patterns. Currently, there looks to be between 1 billion to 2 billion cubic feet per day of production shut in in northern Appalachia due to low prices. This again will be a burden on supply once it is released, unless of course cold weather in the area can take away supplies.

FIGURE 1

Natural Gas Price Trends (2020-24)

The Mountain Valley Pipeline and Plaquemines LNG export facility in Louisiana will help, but not at the level that is needed with additional production. Plaquemines is expected to come online in the first quarter and will move as much as 2.6 Bcf/d of LNG out of the U.S. market and into other countries.

Nevertheless, we believe natural gas prices in the low $2 range are too cheap and that higher prices are to come. Prices setting just north of $3.00 in the first quarter 2025 and at $2.90 in the second quarter are fairly priced, but through the end of December, cold winter weather had largely failed to materialize. Colder-than-normal temperatures in January and February could easily propel prices north of $3.50 and potentially even higher should geopolitical escalations occur to constrain global supplies.

The last half of 2025 is currently priced at $3.30/MMBtu, but any significant weather demand could easily propel prices to $4.00 or even $4.50 by the end of 2025. That said, this price forecast is dependent on the U.S. economy remaining in a soft-landing mode, as industrial demand will be a key factor in rising prices. LNG will help, but could underperform if Russia continues LNG export flows into Europe.

Crude Oil

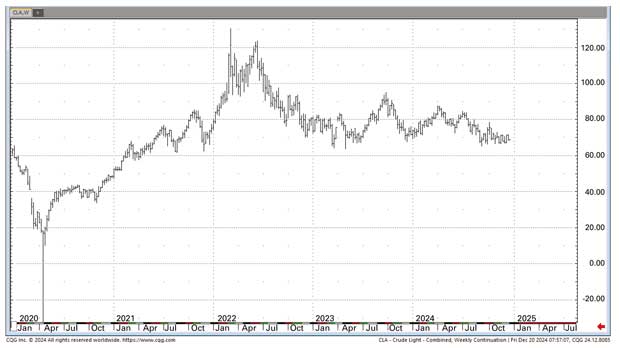

In the final stretch of 2024, oil prices were in a battle between slacking demand from China applying downward pressure and geopolitical tension (in the Middle East and between Ukraine and Russia) applying upward pressure (Figure 2). Many analysts believe that at the current economic pace of China, crude will very likely be in an “oversupply situation” if we see OPEC increase production in 2025. However, if Saudi Aramco’s current quarterly dividend payouts are exceeding cash generation and placing them in a debt situation when Brent prices are below $75/bbl, one would think they would be lobbying heavily not to increase production.

FIGURE 2

Crude Oil Price Trends (2020-24)

The biggest wildcard going into 2025 will be Iran’s relationship with other world leaders if war efforts continue to escalate with Israel. Keep in mind that Iran exports nearly 1.8 MMbbl/d. If its oil infrastructure is damaged, it potentially could result in a quick WTI price spike to the $90/bbl area. However, this would likely be short lived, as the rest of OPEC probably would be happy to fill the void, especially at higher prices.

WTI crude futures continue to consolidate between $63/bbl and $79/bbl. This sideways action probably will continue. However, geopolitical wildcards are very relevant and the consolidation of companies in the production industry will go on. Altogether, this should mean leaner operations that are even more price sensitive, and more constrained supplies at lower prices. More production with less will be the name of the game, which should keep a positive tone for oil and gas stockholders.

M&A and A&D

Following suit with 2024 trends, preserving the balance sheet and securing a return on capital remain the primary goals for exploration and production companies in 2025.

In the first nine months of 2024, U.S. oil production increased by less than 2%, while gas production remained flat. This slowdown in production was because of a combination of consolidation, operators adhering to investor desire for limited to no growth, capital discipline, and production curtailment led by natural gas producers.

In addition, the rig count continued to decline, to reach a three-year low in the last quarter of 2024. Two years ago, we saw private operators dominating the rig scene as they drilled toward sale. With consolidation and buyers dropping rigs, public companies have taken over, contributing to a more predictable commodity market.

Despite lower rig counts, U.S. producers were able to maintain record crude oil and natural gas production through drilling and completions efficiencies via new drilling technologies, extended-length laterals, completion optimization, and production enhancements. Assuming we do not see any drastic price swings because of further escalation of existing conflicts, material changes are not expected in production or the number of active rigs in 2025.

Debt levels remain healthy. Similarly, capital expenditures and reinvestment rates showed no material changes in 2024. In the last two years, public companies spent around 60% of their cash flows, on average, from operations and returned the balance to shareholders through buybacks and dividends. Public companies will remain disciplined and in “development mode” following investor demands.

With a few exceptions (some majors and natural gas operators), E&P companies’ trading multiples remain compressed to three to five times earnings before interest, taxes, depreciation and amortization (EBITDA). Operating cash flows have been steady, and companies continued to generate cash, but the sector will have to perform for a while to drive multiple expansion. In 2024, the energy sector underperformed the S&P 500 by about 20% in comparison.

More consolidation is anticipated in the new year, but not at 2023 values as the list of targets is shrinking. The motivation has not changed with publics looking for scale and duration to stay relevant.

Acquisition and divestiture activity at the asset level was higher in 2024 than it had been in 2023 and in line with 2021 and 2022, but the deal count stayed below pre-2023. In general, acquiring entities prioritized digesting the mergers and realizing synergies, showing a lack of urgency to shed non-core assets. Healthy balance sheets, the limited use of proceeds, and regulatory delays were also to blame for the low asset supply. Assuming no extreme price volatility, deal flow should increase in 2025.

Energy Transition

Finally, 2024 saw a slowdown in the push for alternative energy in favor of natural gas. There has been a change of mentality that has come with the realization that new energy sources complement, as opposed to replace, traditional energy sources and that net zero will not happen without oil and gas.

Energy diversity and energy security are both key focuses of governments post-Russia/Ukraine war. President-elect Trump obviously advocated an “all the above” approach to energy development in his first term, and his new administration is expected to demonstrate equally strong support for both oil and gas.

Going forward, the industry, investors, and governments will need alignment to move to a cleaner energy environment that does not price consumers out. The objective is to create the conditions for economic growth while helping people continue toward a goal of net zero carbon emissions. Investment in clean energy is still largely coming from OECD countries and China, with funding from other countries falling short.

The energy sector sits at the center of generative artificial intelligence, which requires large quantities of clean and reliable power and a resilient grid, and represents a tailwind for natural gas. Natural gas has a lot of advantages with respect to alternative sources of energy, including nuclear. It is inexpensive compared to others, readily available, has low startup costs, and is the more practical solution for powering data centers. We expect to see a continued demand-pull for gas in the coming years to cover the increasing energy needs of AI.

DENNIS KISSLER is senior vice president of trading for BOK Financial, where he has spent more than a decade specializing in analytical research and trading oil and gas futures and derivatives. He has 12 years of experience on the CME trading floor as an independent trader, owned a major commodities brokerage firm with offices in six states, and spent his college summers working on an oil and gas drilling rig in western Oklahoma.

CRISTINA STELLAR is the managing director of energy investment banking for BOK Financial. She holds a master’s in petroleum engineering from the University of Texas at Austin and bachelor’s degrees in both economics and business administration from Charles III University of Madrid.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.