Major Market Drivers Support Upward Pressure On Wintertime Gas Prices

By Dena E. Wiggins

WASHINGTON–Even though U.S. natural gas production is forecast to increase by 4% year-over-year this winter, the Natural Gas Supply Association’s annual Winter Outlook projects upward pressure on natural gas prices compared with the 2021-22 heating season mainly because of the combination of below-average storage and an estimated 2% increase in overall demand.

The NGSA report projects that both natural gas demand and production will expand this winter, thanks to the recovering U.S. economy, a strong global commodity market and higher wellhead prices stimulating increased domestic production.

With a surety of supply, U.S. natural gas prices remain exponentially lower than prices in Europe and Asia, where European geopolitical tensions continue to result in fuel reliability concerns for natural gas as well as coal and oil supply in international markets, driving increased price volatility. While the NGSA analysis does not project wholesale or retail prices, U.S. natural gas prices are starting this winter trading at levels significantly higher than at the start of last winter. Henry Hub prices averaged $4.51 per MMBtu on the New York Mercantile Exchange between Nov. 1, 2021, and March 30, 2022. Late last summer, Henry Hub prices briefly touched double-digit values and entered the 2022 Thanksgiving holiday week trading between $6.75/MMBtu (December futures) and $7.17/MMBtu (January futures) on NYMEX.

The Outlook shows that producers are rising to the challenge of strong winter demand for natural gas at home while meeting the critical needs of an undersupplied global market. European and Asian markets have repeatedly hit seasonal records for regional natural gas prices, a trend that began before Russia’s invasion of Ukraine earlier this year, accelerated after the invasion and then improved somewhat with the arrival of more U.S. LNG cargoes in Europe. Both the U.S. and global gas markets have evolved considerably since NGSA issued its first annual heating season outlook ahead of the 2001-02 winter. During only the past 10 years, domestic gas production has increased by 40%, U.S. consumption has grown 22%, and total U.S. natural gas exports are up more than threefold since Gulf Coast terminals accounting for about 13 Bcf/d of LNG export capacity have entered service since 2016.

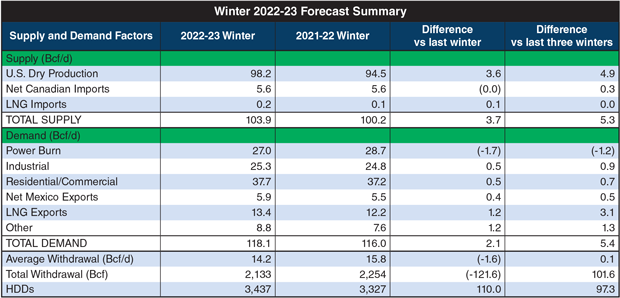

Domestic gas production averaged 4.7 Bcf/d higher last winter than it had the previous winter, with most of that growth coming in the form of Permian associated gas and Haynesville dry gas. This winter, production is forecast to jump another 3.6 Bcf/d to average a record 98.2 Bcf/d, again driven by gains in Haynesville dry gas and Permian associated gas.

Overall, U.S. natural gas markets are expected to remain tight assuming normal winter conditions. Low coal stockpiles and skyrocketing coal prices have countered higher natural gas prices in power generation, ultimately limiting switching between coal and natural gas. Despite higher gas prices, high electric demand supported gas-fired generation last summer. However, given regional gas forward market prices, coal-fired and oil-fired generation will play a critical role this heating season.

Solid LNG demand overseas will also keep U.S. LNG terminals operating at or above nameplate capacity. Beyond that, U.S. LNG exporting capacity should remain steady around 13.5 Bcf/d once Freeport LNG swings back into service as expected in January.

Five Key Areas

The analysis examines publicly available data relating to five key areas: economic indicators, weather, demand, natural gas production and storage. Although each of these potential pressure points is identified separately, all of them are interrelated. Any significant deviation of a single pressure point is likely to affect the other assumptions in the supply and demand equation. The analysis provides an indication of whether market pressures on natural gas prices will be upward, downward or neutral compared with the previous winter.

FIGURE 1

This year’s Winter Outlook forecasts upward price pressure from three of the five areas (Figure 1):

- Weather, with long-range forecasts trending 3.3% colder than last winter;

- Overall demand, with domestic gas demand anticipated to grow 2% year- over-year to average 118.1 Bcf/d from the start of November through the end of March, led by both pipeline and LNG exports as well as the industrial sector; and

- Storage, with U.S. inventories forecast to enter the winter 9% below the five-year average and considerably below the same point last winter.

On the other hand, downward pressure is expected from two areas:

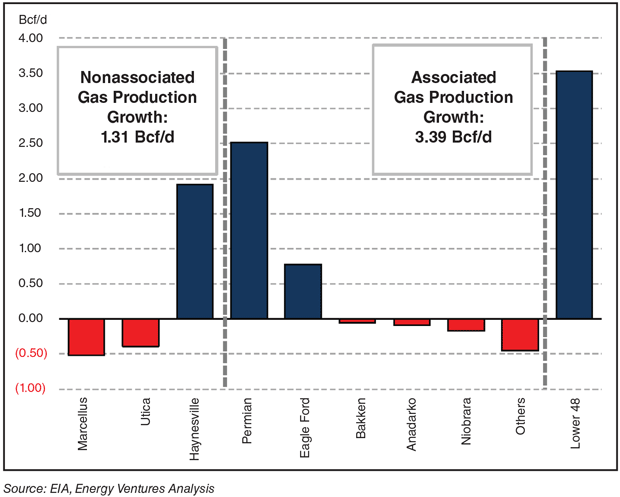

- Supply-side growth resulting in a 4% increase in domestic gas production, driven by output gains primarily in the Haynesville Shale and associated gas from Permian Basin tight oil plays (Figure 2); and

- An economic slowdown, with gross domestic product growth forecast to decline by 0.05% this winter.

FIGURE 2

Gas Production Change by Basin (Summer 2022 versus 2021)

In addition to these key areas, other factors are weighing in on expectations for the market this winter. For example, 2023 will be a banner year for changes in the power generation mix, with 55 gigawatts of new natural gas and renewable resource capacity expected to enter service. These changes make additional natural gas pipeline takeaway capacity even more imperative so that quick-ramping natural gas can be available to provide balance and reliability to the power grid.

Supply Growth Expected

Although higher overall market prices for both oil and natural should incentivize more domestic drilling, limited takeaway capacity, increased price volatility, the ongoing conflict in Europe, and uncertainty around permitting processes and how environmental, social and governance concerns will be factored into future investments are clouding the long-term supply potential. Therefore, moderate near-term production growth is expected as North American producers stick to financial discipline to avoid overinvestment.

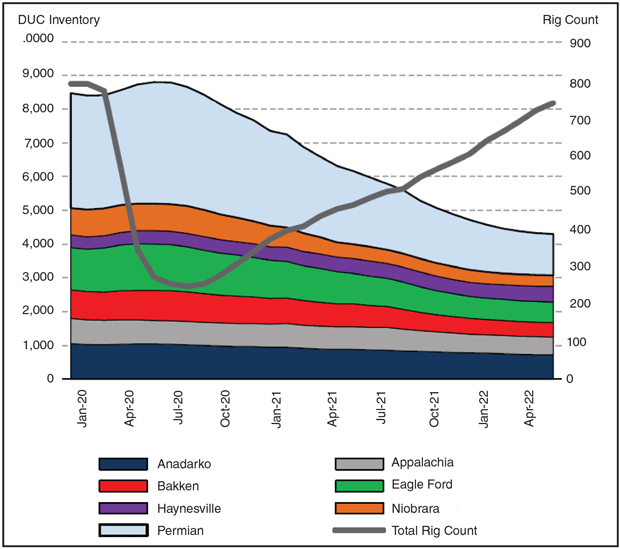

While stronger prices are likely to incentivize new well drilling in the short term, the ability to bring production on quickly is somewhat limited by the steady decline of the number of drilled, but uncompleted wells in inventory. The number of DUCs has been falling at a 4% monthly rate since April 2021, incentivizing the new drilling necessary to maintain or expand current output. The decline in the DUC inventory is yet another indicator of increased natural gas activity (Figure 3).

FIGURE 3

DUC Inventory versus Rig Count

U.S. gas-weighted producers are forecast to increase capital expenditures by 30% in 2022 while oil-focused producers are expected to raise spending by 17%. However, with inflation and the ongoing decline in DUCs, capital spending may support only moderate production growth—albeit at levels sufficient to support record production volumes.

The development of takeaway capacity also plays a role in investment levels. The certification of new gas projects, including pipelines and LNG terminals, will be subject to greater scrutiny if the Federal Energy Regulatory Commission finalizes its certificate and greenhouse gas emissions policy statements in its current problematic forms that require the consideration of difficult-to-quantify indirect and cumulative GHG emissions.

The 2 Bcf/d Mountain Valley Pipeline, already 94% complete, faced increased regulatory challenges after the federal court revoked a key permit in early 2022. Because of the delay, Northeast customers will not benefit from the cost reductions associated with MVP this winter. The mid-term Northeast gas production outlook will largely hinge on the completion of this project.

Robust production growth in the Permian will also test the takeaway capacity limit in the next two years. Major pipelines Agua Blanca (1.8 Bcf/d), Gulf Coast Express (2 Bcf/d) and Whistler (2 Bcf/d) completed over the past three years were more than 90% utilized in 2021. However, some 6 Bcf/d of regional takeaway pipeline projects remain on hold while the market sorts them out.

Demand Drivers

Looking at the power generation sector, nearly 17 gigawatts of coal capacity are being retired in 2002 while 10 GWs of gas-fired units are being added–the biggest annual capacity shift for each resource category since 2019.

Looking back at the summer months, despite much higher Henry Hub prices, dispatch cost competition between gas-fired and coal-fired generation was tighter than expected due to rising coal costs. Higher prices for replacement coal will keep the competition between coal and gas tight this winter, especially in the eastern part of the country where coal prices are up fivefold year over year. Coal stockpiles have not recovered despite the strong utilization of gas-fired generation displacing coal-fired generation. Given the current state of the U.S. coal market, coal plant dispatch is likely to be limited in 2023. One wild card is the potential for a rail strike, which may impact coal deliverability.

The estimated weather-normalized power burn outlook for this winter is 1.9 Bcf/d below last winter, although this decline largely will be offset by higher industrial demand and LNG exports. Comparing this winter with a 2015 baseline, a gain of 6.8 Bcf/d of long-term structural demand growth from new combined-cycle gas units (CCGT) will be offset by a short-term decline of 3.7 Bcf/d.

Renewables saw major growth in 2022, with nearly 45 GW of new wind, solar and battery storage resources. Going forward, it will be essential to ensure that gas-fired generators have sufficient infrastructure to provide the flexibility needed to accommodate the higher ramping requirements of the growing number of variable resources coming on line.

FIGURE 4

U.S. LNG Exports by Destination

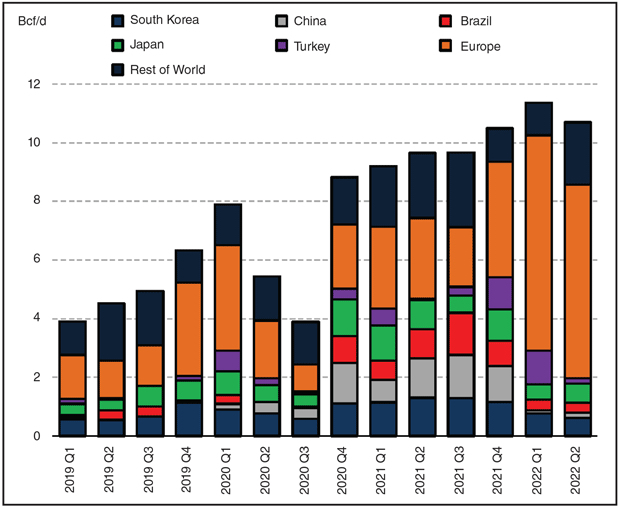

U.S. LNG has become an increasingly important strategic energy source in Europe (Figure 4). The percentages of U.S. LNG cargoes flowing to Europe expanded from 18% in the third quarter of 2021 to more than 50% in the first quarter of 2022, as European gas prices gained strength on Russian supply risk, trading at a premium above the Asian LNG benchmark JKM.

As of March, seven projects totaling 12.8 Bcf/d of exporting capacity were operating or currently undergoing commissioning. The Freeport LNG plant was forced off line after a fire last summer. The facility is expected to restart in mid-December, restoring its 2.1 Bcf/d of liquefaction and export capacity by January. U.S. LNG feed gas demand is expected to average 13.4 Bcf/d this winter with Freeport’s scheduled restart.

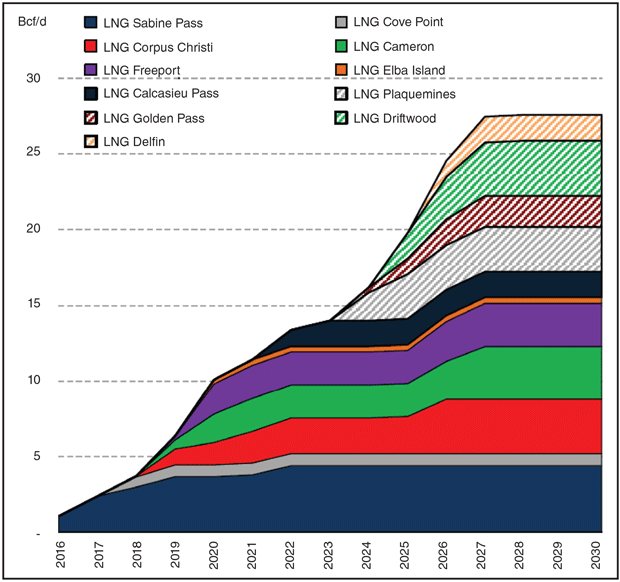

FIGURE 5

U.S. LNG Capacity Development (Through 2030)

Based on the current forward market settlements, estimated netbacks of U.S. LNG exports to Northwest Europe and Northeast Asia remain above $30/MMBtu through 2023. In the near term, U.S. LNG feed gas demand will be constrained by nameplate capacity, and the next major expansion in LNG capacity is not expected until 2024-25 (Figure 5).

Industrial natural gas demand remains strong. Despite the increased risk of demand destruction from high natural gas prices, the growth of industrial activity will likely continue as manufacturers try to ease the bottlenecks in the supply chain. Moreover, the lower cost of U.S. natural gas relative to international prices gives U.S. customers a competitive advantage.

A total of 46 new industrial projects came on line from 2017 through 2021, solidifying 1.2 Bcf/d of natural gas demand. As a result of the shale revolution and its impact on domestic natural gas prices, the United States is projected to continue to see tremendous long-term growth in industrial demand through 2025. A total of $32 billion is expected to be invested in an additional 22 projects scheduled to come on line between 2022 and 2025: 18 new industrial projects, three plant expapansions and one facility restart. Together, these 22 projects will add another potential 1.0 Bcf/d of incremental demand.

A final demand factor is U.S. gas exports into Mexico, which have increased by 40% over the past five years, reaching 5.9 Bcf/d in 2021. The United States has become a critical supplier to the Mexican power generation sector as cross-border takeaway capacity expansions have improved utilization of downstream pipelines. A case in point is TC Energy’s pending planned startup of the Villa de Reyes pipeline, allowing U.S. gas to reach Central Mexico power plants and industrial facilities. This project further improves the utilization rate on the Sur de Texas-Tuxpan pipeline that draws gas from the Permian.

Editor’s Note: The preceding article was adapted from the Natural Gas Supply Association’s 22nd annual Winter Outlook report, which was developed using data from Energy Ventures Analysis Inc., the U.S. Energy Information Administration, Moody’s Analytics and other sources. NGSA does not project wholesale or retail market prices.

DENA E. WIGGINS is president and chief executive officer of the Natural Gas Supply Association, leading NGSA’s efforts to advance the natural gas industry’s economic and environmental agenda with member companies, regulators, legislators and other key stakeholders. Wiggins has spent much of her professional career engaged in representing producer/marketers before the Federal Energy Regulatory Commission, and has been involved in every major natural gas rulemaking since Order No. 436. She is deeply involved in the National Association of Regulatory Utility Commissioners, particularly the Committee on Gas, where she has advocated for the benefits of natural gas in a lower-carbon energy future. Prior to NGSA, Wiggins was a partner in the law firm of Ballard Spahr and served as general counsel to the Process Gas Consumers Group. She holds a B.A. from the University of Richmond and a J.D. from Georgetown University Law Center.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.