Unconventional Gas Supplies Create Golden Opportunity To Reshape U.S. Energy Policy

By David A. Trice

HOUSTON–There has been a sea change in the North American energy market that is forcing electric utilities, major domestic industries and policymakers to rethink basic assumptions about the nation’s energy future. New, abundant supplies of natural gas–made available by technological breakthroughs in exploration and production–have transformed the opportunity and outlook for natural gas in terms of reliability, pricing elasticity and economic impact.

This game-changing “new” natural gas also has the potential to rapidly reduce the carbon-intensity of North America’s economy, slashing carbon emissions by millions of tons while contributing to both economic growth and environmental goals.

We are quite literally entering a new era of discovery for North American natural gas. New shale gas plays have dramatically increased the near- and long-term availability of natural gas supply. These huge onshore supplies are serving to augment and diversify production from offshore sources, and the two together have created a new and more stabilized price dynamic. For the first time, North America is able to consider a myriad of possibilities for this clean fuel, including transportation and base-load power generation.

Only a few years ago, the idea of domestic demand growing to more than 30 trillion cubic feet annually by 2020–which had been rather famously projected by the U.S. Department of Energy in 1999–seemed out of the question, even if North American production was augmented by the development of Arctic reserves and large volumes of liquefied natural gas imports. Access to new places to drill was the industry’s number one issue as producers sought to enter the eastern Gulf of Mexico and onshore areas in the western U.S. to search for new reserves.

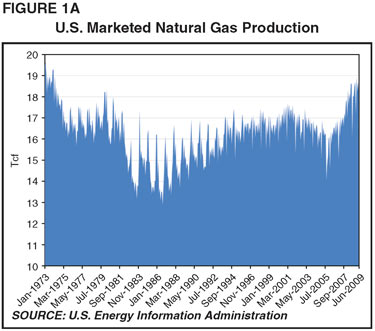

But since 2005, the development of natural gas from unconventional resources–particularly shales–has exploded. After years of “holding the line” on gas production between 19 trillion and 20 trillion cubic feet, total U.S. marketed production jumped to 21.4 Tcf in 2008–the highest output since 1974. Last June, the Potential Gas Committee assessed technically recoverable resources at 1,836 Tcf, representing an increase of 35 percent over its previous estimate.

Suddenly, growing domestic supply to meet a 30 Tcf market seems achievable, thanks to the application of horizontal drilling and multistage hydraulic fracture stimulations in ultralow-permeability shale and tight-sand reservoirs. Indeed, these technologies have doubled the resource in the past five years and are expected to double them again within the next five years.

Just like that, the market went from one of general supply tightness to one with huge new supply additions. Gone are the concerns about shortages and extreme price volatility that squeezed “low-margin” consumers such as fertilizer manufacturers out of the market. At the moment, there is too much gas crowding the delivery system. The supply build, combined with reduced consumption in a recessed economy, has driven prices to seven-year lows, slashed drilling margins and temporarily removed much of the economic incentive that spurred unconventional gas development in the first place.

Natural gas producers–primarily U.S.-based independents–have proven up the concept of unconventional natural gas, and in doing so, have also proven that the United States has a plentiful supply of an affordable and clean energy resource right here at home.

This new reality in North American supply has occurred with amazing swiftness, and this sudden paradigm shift is not yet appreciated by policymakers or a public conditioned to old ways of thinking (i.e., resource constraints and high prices). That is understandable, considering that the productivity of unconventional gas has surprised everyone–including those in the business of producing gas.

Golden Opportunity

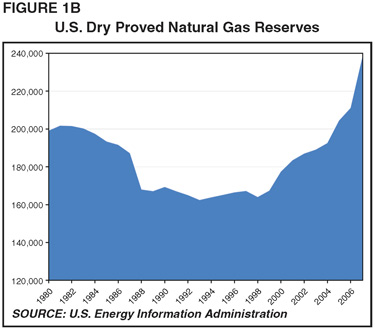

Independent producers have done what many once thought impossible in growing production and reserves (Figures 1A and 1B). In doing so, they have presented the nation with a golden opportunity to take advantage of the newfound abundance of natural gas to reshape energy policy. The next step is for consumption to expand in key sectors in order for the United States to reap the full economic, environmental and national security benefits associated with natural gas.

The shale gas era began in the Barnett Shale with the pioneering work performed by George Mitchell and his company, Mitchell Energy & Development Corp. Mitchell had been experimenting in the Barnett for years, but the play did not take off commercially until after 2001, when higher commodity prices made it possible to experiment with stimulation and horizontal drilling techniques. As Mitchell (and then Devon Energy Corp., which acquired Mitchell Energy in 2002) learned more about the shale and how to drill and stimulate it, the Barnett became both repeatable and profitable.

By 2006, Barnett operators were drilling almost exclusively horizontally, with longer laterals and more stimulation stages with higher frac densities. Initial productivity rates soared, and production from the play exploded from 100 million cubic feet a day in 2001 to 4.5 billion cubic feet a day in 2008–accounting for more than 6 percent of total U.S. supply.

On the heels of success in the Barnett, the industry went searching for the next big shale play. What it found was not one more shale, but many of them–along with many prospective tight sands.

Applying the lessons learned in the Barnett to economically develop reserves in new shales and tight sands is the force behind the gains in U.S. gas production. The same technologies and methods developed in the Barnett Shale now are being applied with equal success to increase production rates, lower unit costs and improve well recovery in other plays.

The fundamental game changer with these plays is scale. North America is a mature province for conventional natural gas. Field size tends to decrease over time as an area matures, and the average field in the United States covered only a few hundred acres. On the other hand, unconventional formations are “blanket” geologic features that can cover millions of acres. The Marcellus Shale, for instance, is estimated to encompass 65 million acres, spanning a large and nearly continuous area from central New York to northern Virginia. Up to 10 horizontal wells can be drilled on a 640-acre section with lateral lengths to 4,000 feet or longer. These plays give operators lots of wells to drill and lots of gas to produce.

Early Stages

The industry is still in the early stages of unconventional gas. There are five main gas shales (Barnett, Haynesville, Woodford, Fayetteville and Marcellus) and one oil shale (Bakken) under active development in the lower-48. There are numerous other shales–both oil and gas–in the United States and Canada, including a number of plays now in the assessment phase where operators are investigating the rock properties, organic contents, etc., to determine commerciality.

Some of these shales may require higher prices than others, and an economic pecking order likely will emerge, whereby the lowest-cost plays are developed first. Numerous plays will be tested, and I believe, ultimately developed, given a sufficient wellhead price.

It is not only shales. Massive potential also exists in tight gas sands, especially in the Rocky Mountains and Mid-Continent. Tight sand plays include giant fields such as the Pinedale Anticline, but also emerging regional-scale trends in historic producing areas with established pipeline and processing infrastructure. An example of the latter is the Granite Wash play in western Oklahoma and the Texas Panhandle. A thick (as much as 3,000-plus feet) package of extremely tight sands, siltstones and shales in stacked sequences, the Pennsylvanian-age Granite Wash reservoir section contains as many as 30 potential pay zones.

Recently, operators have employed the same technologies that have been successful in shale plays in drilling and completing within intervals of the Granite Wash. The early results have been remarkable, with rates comparable to the best shale wells. At Newfield Exploration’s Stiles Ranch Field, for instance, horizontal drilling is resulting in production rates and reserve recoveries averaging three to four times those of multizone vertical wells. The initial productivity rates of Newfield’s first seven horizontals at Stiles Ranch have averaged more than 22 MMcf/d and indications are that each well will each recover ±8 Bcf in reserves. And to date, Newfield has tested only four of 30 potentially productive formations within the Granite Wash at Stiles Ranch.

There are probably 40-50 other tight gas sands plays across the United States and Canada that ultimately will be tested, and a large number of them will be developed commercially at some point. As always, the combination of creativity and technology will continue to be critical in making the economics of these plays work.

Foundational Role

Natural gas has a foundational role for the nation’s energy needs in a global marketplace where concerns about such complex issues as climate change, energy security and growing resource demand are escalating. Unconventional gas provides an unparalleled ability to significantly increase domestic production of a clean and safe energy resource, and to sustain higher production levels for many decades to come.

America’s Natural Gas Alliance (ANGA), an organization formed earlier this year by leading North American independent gas producing companies, is undertaking a study on the size of the U.S. natural gas resource base. Our members are confident that the resource is at least 100 years’ worth of supply and it is growing, but some of the questions we now are examining include how much and how fast production can increase, the price level necessary to sustain growth, and how long it can be sustained.

We are confident that supply growth is not a flash in the pan event, and that natural gas is uniquely positioned as the foundational fuel to a new energy economy. And ANGA is reaching out to Congress to help define the new politics of natural gas, given the unprecedented long-term supply picture.

Adopting a more “gas-centric” approach to U.S. energy policy can only mean good things. Natural gas makes sense not only in terms of national security and environmental stewardship, but increased development of domestic resources also will have a tremendous impact on the national economy, as well on local economies in areas in which tight gas plays are located (shales and tight sands are found in several states, including areas in which oil and gas production activity has been historically limited).

The first-ever study to measure the impact of the natural gas industry (separate from the oil industry) on the U.S. economy shows the industry is responsible for 3 million jobs in the United States, and that 400,000 new jobs were created between 2006 and 2008. The study also found that the natural gas industry contributed $385 billion to the economy in 2008, and more than $190 billion in labor income alone. Natural gas jobs exist in every state except Hawaii, and natural gas is produced in 32 states.

Simply put, instead of sending billions of dollars overseas to pay for imported oil, developing more gas resources within North America would put U.S. citizens to work in high-paying domestic jobs, generate tax revenues, reduce pollution and help balance the trade deficit (the United States spent $25 billion on imported oil in August alone, equating to $564,201 a minute). The truth is that the economic impact associated with unconventional gas development is so persuasive that it gives the industry a decided competitive advantage.

As an illustration, consider a Pennsylvania State University study released in July titled, “An Emerging Giant: Prospects and Economic Impacts of Developing the Marcellus Shale Natural Gas Play.” The study projects that economic output from the play this year will exceed $3.8 billion, state and local tax revenues will be more than $400 million, and total job creation will exceed 48,000.

The study goes on to note that the present value of additional state and local taxes earned from Marcellus development over the next 10 years is almost $12 billion. Moreover, it estimates that by 2020, Marcellus production could hit 4 Bcf/d, generating $13.5 billion in value and nearly 175,000 jobs.

Those kinds of numbers underscore the obvious economic benefits of developing tight gas, and illustrate how these plays represent win/win situations for consumers, producers and government alike.

Own Best Friend

It has been said that producers have been their own worst enemies by bringing a flood of unconventional gas to market during a period of depressed demand, in effect, overwhelming demand and undercutting prices. To the contrary, however, I suggest that producers have been their own best friends by demonstrating that natural gas is abundant and that supply can grow organically with the right price signals. It now is clear that the industry can deliver the gas, but the question is whether the market will be able to take it.

Now that producers have built the supply base, demand must expand to realize the full benefits that natural gas has to offer. Two market sectors represent the greatest growth potential: power generation and long-haul/fleet transportation.

More than 400 gigawatts of gas-fired electric capacity already exists in the United States, but it is used only 20-25 percent of the time for peak demand loads. Going forward, the Energy Information Administration forecasts a 40 percent increase in natural gas consumption in the power generation sector by 2030.

Natural gas is integral to the mandate for renewable energy, and combined-cycle natural gas plants are ideal for backing up wind and solar. Because wind is so intermittent, wind turbines only run at 30 percent efficiency on average. If meaningful carbon cap-and-trade legislation is enacted–that is, legislation that puts energy sources on a level playing field–natural gas demand should increase substantially for power generation.

Driven by the environmental attributes of clean burning natural gas, municipalities have been among the earliest adopters of low emitting natural gas buses and fleet vehicles. However, there is a huge potential market in converting over-the-road diesel trucks to natural gas, as advocated by T. Boone Pickens. These are vehicles that travel 150,000-200,000 miles a year at an average of six or seven miles to the gallon. Converting long-haul trucks to natural gas would dramatically reduce the amount of oil the United States imports, while simultaneously slashing exhaust emissions.

ANGA recognizes that trucking companies will need incentives to help offset the cost of converting fleets, and fueling station infrastructure also will have to be developed, which will require considerable capital investment. Consequently, ANGA supports proposed congressional action to encourage diesel-to-natural gas truck engine conversions and to fund the construction of refueling stations.

The Way Forward

With the right policies in place to capitalize on its environmental, national security and economic advantages, the way forward can include an expanded role for natural gas in the U.S. energy mix. For the consumer, the message is that the country is blessed with abundant gas resources. And not only is natural gas reliable and plentiful, but because so many plays will compete head-to-head for market share, prices will remain reasonable and affordable.

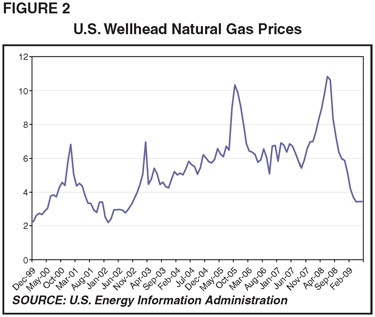

Prices have been unreasonably low in 2009 (Figure 2) and most, if not all, unconventional gas plays are not economic at these low prices. Just as prices that were too high were destructive for demand earlier this decade, prices that are too low are just as damaging to supply in the long term. I believe the market eventually will find a balance in a range of $5-$8 an Mcf. That is equivalent to an oil price range of $30-$48 a barrel, or about half the going oil price.

For the natural gas industry, the implication is clear that the low-cost producer will be the winner–certainly in the stock market. Unlike high risk exploration, unconventional plays are manufacturing operations that rely on engineering. The keys to success for independent producers will be controlling cost and managing risk, even for the best geology located in the best places.

The plays that can have the highest margins (which is related to finding and development costs, and the transportation differential associated with getting the gas to market) will reap the biggest rewards. The most economic plays will capture market share initially, with some of the less economic plays forced to wait for a better day.

For independent producers and operators, the new market fundamentals also point out the need to manage price risk through derivatives and hedging transactions. One troubling development is a provision in the American Clean Energy & Security Act of 2009 (the Waxman-Markey bill) as well as a proposal advocated by U.S. Treasury Secretary Timothy Geithner. Both would require hedges to be cleared through an exchange, and would mandate margin calls and posting collateral. That would be adverse to independent producers, which are not speculators, but hedge purely to manage price risk.

ANGA was formed in March to foster a more balanced approach to U.S. energy policy; one that rightfully puts natural gas at the forefront. Natural gas should be integral to any debate on energy and climate change issues, and the compelling economic benefits of unconventional gas development need to be a big part of the discussion. We have a long road ahead, but the natural gas industry now is being heard by policymakers who are beginning to recognize that natural gas can be the foundation for energy and climate change policy.

Editor’s Note: America’s Natural Gas Alliance (http://www.anga.us) was formed last March by leading independent natural gas exploration and production companies to promote the environmental, economic and national security benefits of domestic natural gas. ANGA’s 28 member companies collectively produce 9 Tcf of natural gas annually, or more than 40 percent of total U.S. supply.

Members companies are Anadarko Petroleum Corporation, Apache Corporation, BHP Billiton, Bill Barrett Corporation, Cabot Oil & Gas Corporation, Chesapeake Energy Corporation, Cimarex Energy Co., Devon Energy Corporation, El Paso Corporation, EnCana, Energen Resources Corporation, EOG Resources Inc., Laredo Petroleum Inc., LINN Energy LLC, Newfield Exploration Company, Noble Energy Inc., Petrohawk Energy Corporation, Pioneer Natural Resources Company, Plains Exploration & Production Company, Questar Exploration & Production Company, Range Resources Corporation, SandRidge Energy Inc., Seneca Resources Corporation, Southwestern Energy Company, St. Mary Land & Exploration Company, Ultra Petroleum Corp., Williams Companies, and XTO Energy Inc.

DAVID A. TRICE is nonexecutive chairman of Newfield Exploration Company and chairman of America’s Natural Gas Alliance. Trice is one of the founders of Newfield Exploration, and recently retired as the company’s chief executive officer. He has also worked as president, CEO and director of Huffco Group Inc., and as an attorney. Trice serves on the board of directors at McDermott International, Hornbeck Offshore Services Inc. and New Jersey Resources. He previously served as chairman of the American Exploration & Production Council, and is on the Houston Museum of Natural Science Board of Trustees.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.