Shale Gas, Tight Oil And EOR Creating Rare Opportunity For Industry And Nation

By Philip H. “Pete” Stark

ENGLEWOOD, CO.–The foundation of any modern economy begins with natural resource development. It was largely because of an abundance of natural resources that the U.S. economy became the envy of the world. Until a few years ago, however, the foundation of domestic oil and gas resources had been slowly eroding, and it was negatively impacting all sectors of the American economy. But with the development of first shale gas and now tight oil, the tide has turned and the U.S. energy picture has been redrawn.

The country now finds itself in position to seize control of its own energy destiny. That would have seemed the unlikeliest of possibilities a decade ago, but huge supplies of oil and natural gas from shales and tight formations are, in effect, turning the clock back to a time when economic growth was fueled by plentiful and affordable domestic energy production. Unconventional resources are creating a once-in-a-lifetime opportunity to redirect the course of the nation’s energy future, and the economic, environmental and national security implications are profound.

Policymakers and the public at large only now are beginning to understand the full measurements of value that shale gas and tight oil development bring on the local, state and national levels. The supply “scarcity” mentality that persisted in U.S. energy markets for years is yielding to a new reality of supply “abundance,” and a growing recognition that the new-found wealth of unconventional resources can serve as a pillar of economic growth for decades to come.

On the natural gas side, the market transformation is epitomized by the almost crying urgency that was perceived for liquefied natural gas imports as recently as 2007. Five years ago, virtually every analyst was forecasting that the United States would today be importing at least 8 billion cubic feet a day of foreign-sourced LNG to satisfy present consumption levels, with future demand growth severely curtailed by high supply costs. With so much imported LNG landing in the domestic market, U.S. natural gas prices today would probably be competitive with world prices in the range of $8-$9 an Mcf, and certainly not $3/Mcf.

Leaving aside for the moment the tremendous impact of the “shale gale” on jobs, royalties and tax payments, by eliminating the need to import large LNG volumes, shale gas has directly eliminated more than $23 billion a year that would have been leaving the country, had the United States been forced to rely on LNG as a major supply source. At the same time, consumers’ natural gas bills have been slashed by 50-70 percent.

The same story is now unfolding in tight oil plays. Of the 19 million barrels of oil a day the United States consumes, about 9 million bbl/d (47 percent) is imported. Over the next decade, we project that North American producers will add 4 million-5 million bbl/d of new production through tight reservoirs, enhanced recovery in mature reservoirs and Canadian oil sands. That equates to backing out roughly 50 percent of foreign-sourced oil imports, which has tremendous economic and national security ramifications. Billions of dollars would be saved annually by simply stemming the flow of dollars that takes place every day between the United States and overseas oil exporting nations–arguably the greatest commercial transfer of wealth the world has ever seen.

Leading The Way

Independent operators have been the catalysts of this energy transformation, leading the way to a new era of unconventional resource plays. In the process, they have created an entirely new dynamic in global oil and gas markets. Completely counter to the 1990s, when the majors were abandoning onshore North America, U.S. and Canadian gas shale and tight oil plays are attracting giant capital investments from major and international companies, who are re-entering North America to partner with the independents that have pioneered these plays.

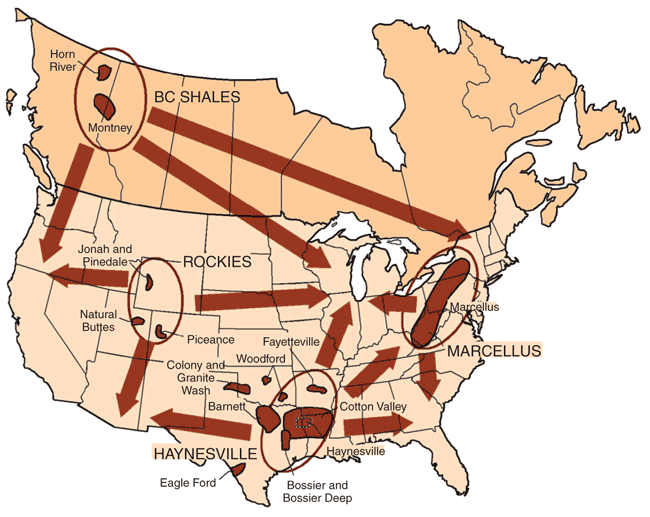

FIGURE 1

Major North American Unconventional Gas Plays

Unconventional resource plays have provided an opportunity for independents to do what they have always done best: exercise ingenuity and apply technology in creative ways. Each successful play has opened one door after another, beginning with George Mitchell and his company’s work to produce economic natural gas volumes from the Barnett Shale. Success in the Barnett led to developing the Fayetteville and Bakken, which in turn, led to new waves of success in the Woodford, Haynesville, Marcellus, Eagle Ford, Horn River, etc. That initial success in the Barnett has opened dozens of resource play opportunities all across the continent (Figure 1).

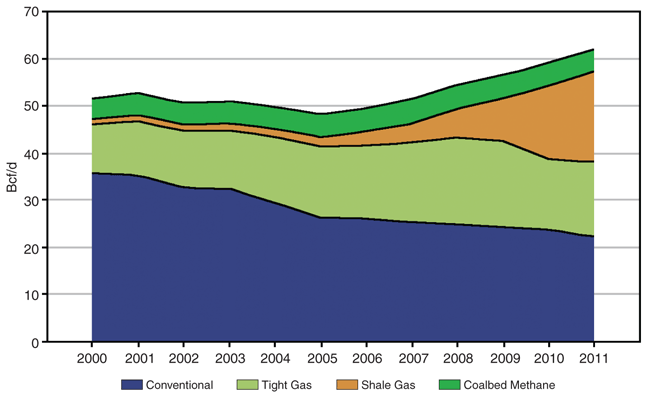

FIGURE 2

Lower-48 Natural Gas Production by Type

(2000-10)

The shale gale for natural gas happened suddenly and production surged rapidly, transforming the domestic industry in only about four years. By early 2008, the market had begun to realize the full magnitude of what independent operators had accomplished in pioneering shale plays, and started to make sense of what shale gas meant to U.S. supply (Figure 2).

For independents, unconventional plays create an entirely new world of business opportunities in their own backyard. However, one of the lessons learned in shale gas is that developing lease positions requires a scale of operations that many smaller and midsized operators simply cannot handle easily, particularly the amounts of capital needed. Consequently, majors, national oil companies and foreign investment firms are making long-term investments in North American shale gas plays. This is injecting billions of dollars into the onshore U.S. and Canadian upstream sectors and is reversing the exodus of capital that followed the majors’ migration from U.S. land operations to deepwater and international areas in the 1990s.

The next wave in North American unconventional resource development is now well under way, and it is creating opportunities to transform the production of oil and natural gas liquids from tight formations on a scale equivalent to the impact of shale plays on gas supply.

The initial phase of the liquids wave began commensurate with the advent of horizontal drilling and multistage completion technology in the Barnett in 2003-04. Bakken operators also adopted horizontal drilling and completion methods during this same period, although it took a while for the technology as applied in the Bakken to be taken up in other tight liquids plays.

The next wave in unconventional resource development is now well under way, and it is creating equal opportunities for transforming the production of oil and natural gas liquids from tight North American formations.

Transitioning To Oil

Unfortunately, the shale gale brought a surge of new supplies to the market right on top of the recession-related demand slump in 2008-09. Independents that had geared up to deliver gas to the marketplace at $6.00-$7.00 an Mcf found themselves receiving a 40-50 percent lower price. Consequently, independents began searching for Bakken-like opportunities, where horizontal drilling and multistage completions could be used to produce higher-value liquids from tight reservoirs in the wet gas and/or oil windows. Over the past two years, both large and small independents have transitioned from an almost exclusive natural gas focus to a mix of oil, gas and NGLs, with drilling activity increasingly targeting oil.

Tight oil plays use the same basic technologies as gas shale plays, and in some cases, even the same reservoir. A case in point is the Eagle Ford, where independents have moved from drilling dry gas when the play emerged in 2008 to first the wet gas window, and then the oil window. In fact, Eagle Ford activity is a perfect analogue for how independents have shifted the impetus from gas to liquids to oil drilling. In the first week of January 2009, almost 80 percent of the 1,623 active U.S. rigs were drilling for natural gas and 20 percent (346 rigs) were targeting oil. By the first week of January 2012, that ratio had changed to 60 percent oil and 40 percent natural gas, with 1,191 of the 2,007 rigs pursuing oil.

In addition, the percentage of rigs drilling horizontally has nearly doubled since October 2008, from 31 to nearly 60 percent, indicating that the majority of the active rig fleet is targeting tight plays. Looking forward, the trend toward horizontal oil drilling shows no discernible signs of slowing, especially with oil priced much higher than gas on a Btu equivalent basis and independents continuing to investigate new tight oil frontiers.

At the same time, independents are leading another very important transition to leverage the same horizontal drilling and multistage frac methods used in tight reservoirs to enhance oil recovery in mature conventional reservoirs. This is happening already in the Permian Basin, where the Clear Fork, San Andres and other formations are targets for drilling horizontal wells to enhance recoveries in waterflood projects and in bypassed reservoirs. Some forward-thinking executives of large U.S. independents believe that combining horizontal drilling and EOR in mature fields may ultimately produce even more new oil than tight reservoirs. It is clear that EOR holds enormous potential, and the industry is on the cusp on realizing that potential today.

Major Advantage

With respect to natural gas, we are facing a period of exceptionally affordable prices, and that is a major advantage that will distinguish the United States in the global economy for decades to come. Affordable energy has been a cornerstone of industrial growth and quality of life throughout the nation’s history, and with shale gas, a large part of future U.S. energy needs will be met at a much lower cost than almost any other region in the world. That could provide a competitive advantage to the entire U.S. economy.

A new IHS Global Insight study measures the economic impact of shale gas development in terms of creating jobs, reducing consumer costs, stimulating economic growth and bolstering federal, state and local tax revenues. The study found that shale gas production supported more than 600,000 jobs in 2010, and is projected to support 870,000 jobs by 2015 and 1.6 million by 2035.

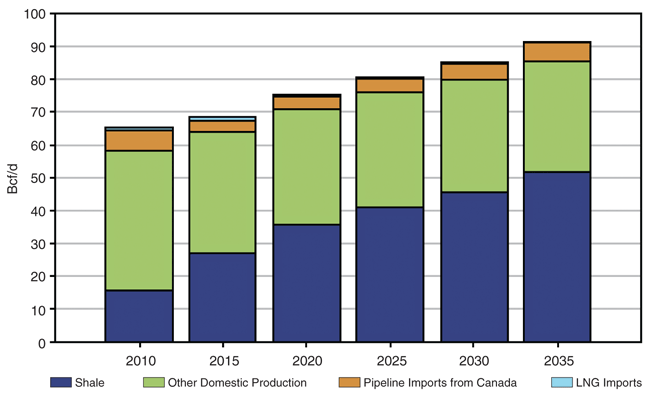

FIGURE 3

Lower-48 Natural Gas Production Forecast

(Through 2035)

By September 2011, shale gas accounted for 34 percent of total U.S. natural gas production, and is forecast to grow to 43 percent in 2015 and 60 percent by 2035 (Figure 3). The study estimates that the industry will invest $1.9 trillion in shale gas projects between 2010 and 2035, with especially strong capital expenditures in the near future growing from $33 billion annually in 2010 to $48 billion in 2015.

Shale gas development contributed more than $76 billion to U.S. gross domestic product in 2010, and should reach $118 billion by 2015 and $231 billion by 2035. Shale gas production contributed $18.6 billion in federal, state and local government tax and federal royalty revenues, and is projected to generate more than $933 billion in federal, state and local tax and royalty revenues over the next 25 years on a cumulative basis.

The study found that the full-cycle cost of shale gas produced from wells drilled in 2011 averaged 40-50 percent less than the cost of gas from conventional wells drilled last year. The liquids component of the shale gas production stream is a major contributor to lower full-cycle costs. This implies that because of the lower cost structure, producers can tolerate a lower wellhead natural gas price and still generate acceptable rates of return. Moderate prices with reduced volatility are, of course, key to growing long-term demand and expanding natural gas markets.

Without shale gas production, relying on high levels of LNG imports would cause U.S. natural gas prices to soar by 200-300 percent. The IHS Global Insight study estimates that lower natural gas prices will result in an average 10 percent reduction in electricity costs nationwide over the next couple decades, adding an average $926 to annual U.S. disposable household income between 2012 and 2015, and more than $2,000 annually per household by 2035. Moreover, lower prices are forecast to result in 2.9 percent higher U.S. industrial production by 2017 and 4.7 percent higher industrial production by 2035.

Even with lower commodity prices, the economic incentive will remain in place to continue drilling shale gas plays, although there will be adjustments. The richest parts of shale gas reservoirs have resulted in initial production rates of 10 million-25 million cubic feet a day. Over the past three years, shale gas wells have reversed what had been a 10-year long slide in average initial production rates for U.S. gas wells. In fact, initial gas well productivities have more than doubled since the end of 2007. Continuous process improvements and technical innovations initiated by leading operators have achieved higher productivities while indisputably demonstrating the supply potential of shale plays.

Remaining Competitive

In early 2010, IHS estimated there were almost 900 trillion cubic feet of shale gas resource in sweet spots that could be produced at 2010 costs of less than $4/Mcf. There has been a fairly strong inflationary increase in drilling and completion costs over the past several months because of surging oil activity, but higher initial productivities and associated liquids are countering the higher costs for shale gas wells.

In the Marcellus, for example, a “good” well two years ago may have had an IP of 5 MMcf-6 MMcf a day. Today, operators are reporting 8 MMcf/d-10 MMcf/d completions. These continuous process improvements and focus on liquids rich parts of shale gas plays are allowing shale gas operators to remain competitive with low gas prices.

The prospect of an affordable and abundant long-term supply of natural gas is a welcomed development for a market that a few years ago was banking on high-cost Arctic gas and foreign LNG to meet demand in a supply-constrained environment. U.S. gas supply is no longer in doubt. Lower-48 gas production has grown by more than 13 billion cubic feet a day since January 2007. In the past two years, producers have met the demands of two colder-than-normal winters and two hotter-than-normal summers while building storage inventories to record levels.

Thanks to supply increases, the long-term outlook includes rather robust demand growth, with U.S. consumption expanding by more than 25 Bcf/d (to more than 90 Bcf/d) by 2035. Most of the projected increase will occur in the power generation sector, where demand is forecast to more than double over the next two decades.

Anytime gas is $4.00 an Mcf or less, there is an opportunity for power generators to switch coal-fired assets to natural gas while generating much lower greenhouse gas emissions. That helps drive additional demand when gas prices are low, and has particularly been a plus given the fact that the economic downturn has kept demand in other consuming sectors below where it otherwise might be.

Moderate prices also are creating demand growth opportunities in the industrial and manufacturing sector. Manufacturing companies–especially petrochemical companies–that depend on gas as a feedstock or heating source are returning to North America after an overseas exodus that began in the early 2000s.

Natural gas liquids have several advantages over oil-based feedstocks for petrochemicals, and there are billions of dollars worth of proposed capital investment projects on the drawing boards that would bring back manufacturing and petrochemical users that have departed the United States for foreign shores.

One potential demand area that is something of a wild card is using natural gas instead of gasoline and diesel to power trucks and automobiles. Natural gas vehicles are common in other parts of the world, but have been used sparingly in the United States, mainly as bus and truck fleets in metropolitan areas. If the spread between oil and natural gas prices remains wide enough, it could stimulate additional demand for natural gas in the transportation sector beyond fleet use.

Tight Oil Revolution

The unconventional revolution that is now occurring on the oil side could essentially double the economic benefits experienced on the gas side. A litany of new tight oil and liquids-rich shale gas plays have been made economic by horizontal drilling and multistage completions at current oil prices: the Bakken, Eagle Ford, Wolfcamp, Granite Wash, Niobrara, Utica Shale, Mississippi Lime, etc. More than a dozen tight oil plays in North America have demonstrated commerciality.

In 2011, two more potentially large plays–the Niobrara and Utica–demonstrated commerciality and further validated the economics of tight oil development models. Moreover, operators are evaluating the productive capacity of tight oil formations in at least a dozen additional plays.

To date, the industry has identified about 50 billion barrels of oil equivalent recoverable reserves from tight U.S. plays. Moreover, operators are implementing continuing process improvements (as in shale gas reservoirs) that generate higher productivities and lower costs, as well as expanding tight oil plays by adding new reservoir targets.

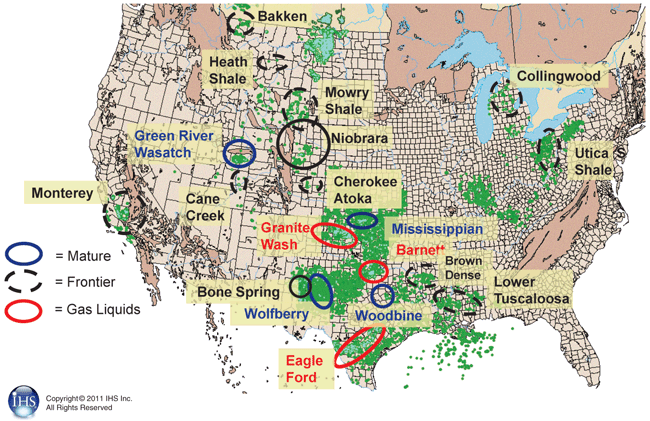

FIGURE 4

Tight, Fine-Grained U.S. Oil Plays

A case in point is the Bakken play, where average per-well peak productivities have increased by 78 percent since 2007. Operators also are adding new components to the reservoir package, most notably zones in the Three Forks formation. Continental Resources announced that three more units of the Three Forks formation are oil-saturated. Those units have not yet been fully tested to demonstrate their potential, but they could indeed be add-on targets for Bakken/Three Forks horizontal wells.

In the Niobrara play, Calcarious-rich Niobrara zones are the prime targets, but Anadarko Petroleum Corp. has announced that it has gone below the Niobrara to complete its first horizontal oil producers in the Codell Sandstone. Two years ago in the Permian Basin, operators were fracturing 1,000-1,500 feet of vertical section in the Spraberry. They now are drilling through the Spraberry into the underlying Wolfcamp and even older rocks to complete 3,000 feet or more with multistage fracs in vertical “Wolfberry” wells.

Similar to shale gas production four or five years ago, tight oil production is growing rapidly. The industry is producing about 700,000 bbl/d in tight oil, primarily from the Bakken Shale and Eagle Ford. IHS projects at least 3 million bbl/d of new onshore U.S. tight oil production by 2020. That is a substantial increase, but the industry is already well on the way toward meeting that target. In 18 months, Eagle Ford production went from essentially zero to more than 140,000 bbl/d, and Bakken production has grown by more than 400,000 bbl/d since 2007.

Amazing To Behold

Even mature basins are experiencing production growth thanks to the development of tight plays. For example, output from the Permian Basin jumped by 75,000 bbl/d during 2010, substantiating a turnaround from a decade-long decline in oil production that lasted from 1998 through 2007. The Permian is getting very close to adding 100,000 bbl/d in annual production, and could rival the Bakken in terms of the rate of daily production growth. Considering how much drilling has occurred in the basin over its 80-year productive history, that kind of turnaround is truly amazing to behold.

The Permian Basin is a reminder that even seemingly mature basins can have significant untapped tight oil potential. However, we also remain very bullish on EOR. In areas such as the Permian, applying horizontal drilling, carbon dioxide flooding and other technologies to boost recovery factors could add tremendous value in many fields and yield significant long-term production increases.

With expanded EOR activity and a projected 1 million bbl/d in Canadian oil sands production, total new North American production may increase by as much as 5 million bbl/d by the end of this decade. That could equate to a $1 trillion contribution to U.S. gross domestic product and an almost equal offset in the balance of payments for oil imports.

Tight oil development is projected to create 1.3 million U.S. jobs by 2020. Moreover, such significant volumes of new production from tight North America reservoirs eventually could dampen global oil price volatility, which would add stability and certainty to U.S. oil prices.

Looking forward, U.S. independents will continue to lead the three-pronged revolution of shale gas, tight oil and EOR. Although the new era in domestic energy development is less than a decade old, it already is making an indelible impact on energy supplies and market factors. Together, shale gas, tight oil and EOR are poised to dramatically alter the nation’s energy future by rebuilding a natural resources foundation that had been in decline for the better part of four decades.

The United States has the rarest of opportunities before it today. With unconventional oil and gas, the nation can reset its economy to take advantage of vast new supplies of domestic energy. Just as billions of dollars are lining up behind the U.S. manufacturing sector based on affordable natural gas supplies, similar investments will happen on the oil side to capitalize on a resurgence in domestic crude output.

The biggest issues for policymakers are fully comprehending the game-changing benefits of increased domestic production, and ensuring that policies are in place to enable these resources to drive U.S. prosperity and security going forward, exactly as they did in the not-too-distant past.

PHILIP H. "PETE" STARK is vice president, industry relations, at IHS in Englewood, Co. Prior to joining IHS in 1969, Stark was an exploration geologist for Mobil Oil. He has authored papers on exploration and production databases, hydrocarbon shows, horizontal drilling, global oil and gas resources, global upstream trends, giant fields, unconventional plays, and U.S. natural gas productivity and supplies. Stark is a 2012 recipient of the American Association of Petroleum Geologists Honorary Member Award. He serves on the boards of the AAPG International Pavilion and the Western Energy Alliance. He also serves on AAPG’s Corporate Advisory Board and Resources Committee. Previously, Stark was chairman of the Board of Visitors for the University of Wisconsin’s department of geology and geophysics. He holds a B.S. in geology from the University of Oklahoma, and an M.S. and a Ph.D. in geology from the University of Wisconsin.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.