Report: Industry Enters Favorable Era

HOUSTON–Noting the unprecedented cyclical changes through which the U.S. oil and gas industry has navigated during the past decade, a new report from Deloitte’s energy, resources and industrials segment determines that, even amid economic uncertainty, geopolitical instability and ongoing supply chain disruptions, the industry is financially strong and poised to drive change.

The analysis, “Striking the Balance: How and Where Will O&G Producers Deploy their Cash?” examines how oil and gas companies can play a key role during the next decade in harmonizing energy security with the energy future, while helping commercialize essential low-carbon technologies.

Deloitte observes that industry disruptions during the past couple years–including shifts in consumer behavior and supply chain challenges–combined with years of underinvestment and producers’ financial discipline, have pushed oil prices higher and expanded companies’ cash flows signficantly. According to the study, the ongoing energy readjustment is likely to keep prices elevated for a while, possibly resulting in record cash flows and helping the industry to strike a healthy balance between energy security, diversification and transition.

Vanishing Debt?

The analysis offers a number of key observations:

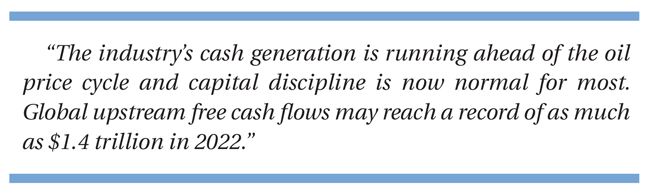

- The industry’s cash generation is running ahead of the oil price cycle and capital discipline is now normal for most.

- Global upstream free cash flows may reach a record of as much as $1.4 trillion in 2022.

- Although losses associated with shale plays limited free cash flow in the North American upstream industry to only $47 billion during 2010-2020, the industry is on pace to generate as much as $600 billion in free cash flow between 2021 and 2022, a 13-fold increase from the aforementioned interval.

- Shale producers, who generated negative cash flows in nine of the last 10 years, likely will witness record-high free cash flows in 2021-2022 that may overcome the decade long loss of $300 billion.

According to Deloitte, the industry has been reducing debt, increasing efficiency and practicing capital discipline for the past six years. After economic uncertainty has prompted companies to pause re-investments, the oil and gas industry is exhibiting exceptional financial health and industry-leading returns at 20% leverage and 4%-6% of dividend yield. Even amid ongoing price volatility and supply chain disruption, many companies are strongly positioned for the future, though defining the road ahead will take time.

The report goes on to suggest that significant investments may be required to strike a careful energy balance. According to the study, $3.6 trillion is the projected hydrocarbon capital expenditure at base price to maintain global operations and generate significant cash flows from 2022 to 2030. However, the study also predicts these investments will compete with growing priorities on cash, including shareholder payouts, buybacks and debt repayment. Even after meeting both core hydrocarbon investment and shareholder priorities, Deloitte forecasts, the global upstream industry is likely to generate $1.5 trillion in cash surplus between 2022 and 2030.

The cash surplus of $1.5 trillion can be deployed in several ways, the firm says, noting that it may “move the needle on the industry’s share of green capex from its current 5% to as much as 30%, it could potentially kickstart the low-carbon economy, or it could be used to technically make the industry completely debt-free.”

Moreover, Deloitte continues, relatively lower internal rate of return investments in low carbon technologies may reduce the overall corporate IRR of an oil and gas company by 2.5%-4.0%. “However, even with that investment, the industry’s overall return profile could remain strong and close to previous highs, in addition to the added benefits of a lower emissions profile,” the firm assesses.

In fact, the report indicates, the industry has been accelerating its low-carbon commitments despite its reputation for volatility. For example, the firm details, during the last three years, many oil and gas companies have slashed direct carbon emissions by 50%. Further, it observes, oil and gas companies account for 75% of the global investment in carbon capture, utilization and storage in 2021, and have doubled their renewable capacity in three years.

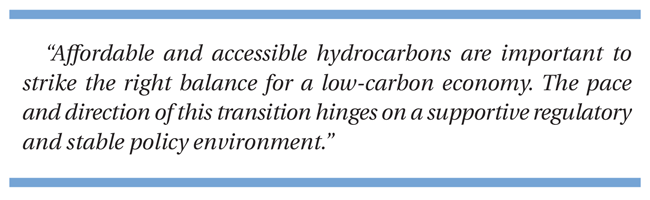

According to the study, affordable and accessible hydrocarbons are important to strike the right balance for a low-carbon economy. The pace and direction of this transition hinges on a supportive regulatory and stable policy environment, coordinated partnerships and innovative business models.

“The oil and gas industry has faced real disruption over the past few years, some of which originated long before the Covid-19 pandemic began to make its impact,” assesses Amy Chronis, vice chair, Deloitte Ltd.’s U.S. oil, gas and chemicals leader. “However, the unexpected result of this volatility is that the industry seems to be in a relatively strong position. Oil and gas companies have managed through change. Those who invest in new business models and remain resilient to the changing market dynamics will be more likely to sustain, lead and win throughout this energy transition.”

“Oil and gas companies are facing a readjustment in the broader energy market,” says John England, Deloitte Touche Tohmatsu Ltd.’s global oil, gas and chemicals leader. “Many companies have already committed to reducing carbon emissions and are making progress, amid geopolitical and economic uncertainty.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.