Public And Private Capital Showing Renewed Favor For Oil And Gas Sector

By Gregory DL Morris, Special Correspondent

Two notable public market transactions at the start of 2025 set expectations for a strong year in capital formation for all types of funding across the oil and gas industry. In mid-January, Plains All American Pipeline announced it had raised $1 billion in 5.95% senior unsecured 10-year notes to fund bolt-on acquisitions. Two weeks later, Infinity Natural Resources said it raised $265 million in its initial public offering. The Appalachian producer is backed by Pearl Energy Investments and NGP, which retain control.

“We were among the underwriters for the Infinity IPO,” says Keith Behrens, head of the energy group at Stephens Investment Banking. “It went very well, and there could be others. There are opportunities if you are of scale and have a good story. On the private side of capital, private equity has been a little soft over the past few years, but that has perked up. There seems to be quite a bit of private equity available to the upstream, especially for backing proven management teams.”

The energy group has been focused on family offices lately, Behrens notes. “That is not a new source, but there are new family offices that have entered the sector, and we are seeing quite a bit of capital from there. We are actively bringing those into our deals.”

The Plains All American Pipeline offering demonstrated that public debt markets are open for energy, but they aren’t the only sources of lending, Behrens says. “Some banks that had gone away have come back,” he assesses. “We focus on unitranche, but there is a lot of dry powder available in all types.”

Returning to the Infinity IPO, Brad Nelson—managing director and head of acquisitions and divestitures in the Stephens Energy Group—notes that for the last few years the public energy companies were primarily yieldcos (companies that own operating assets actively producing predictable cash flows) with growth as a secondary benefit.

“Infinity was an old-school IPO with a growth focus. That message was well received by the market,” Nelson says.

While there have been some complex transactions, for the most part, acquisitions and divestitures are being done as conventional cash plus stock deals, Nelson explains. “Corporate-level mergers and acquisitions imply that the buyer has the balance sheet to absorb the acquisition’s debt.”

The stage of the cycle is an important factor in the volume of business being transacted. “Whenever there is a mega deal done, there are going to be members of management that take the opportunity to go out on their own,” Behrens says. “It is also logical that there are non-core assets that the buyer does not want. Those asset packages are already starting to fall out of the big corporate deals. That will likely continue to happen over the next year or so, especially if operations continue to get commodity price support.”

The shift in gas prices is an important theme, Nelson avers. “A lot of people are now looking at gassy deals. Everyone is aware of the cold winter, liquified natural gas exports, and the expected demand from artificial intelligence centers.”

Turning Tide

The industry is finally coming out of what has been a very difficult fundraising period for private equity within oil and gas, observes J.P. Hanson, global head of Houlihan Lokey’s oil and gas group. “Within the past six months, the tide has very much changed, and we have seen some large private equity funds raised,” he says. “We have finally seen dedicated capital return to fund opportunities within the oil and gas industry. One of the most dedicated private equity funds, EnCap, closed a $6.5 billion fund. I understand it ended up oversubscribed at $6.8 billion.”

He also points out that Quantum Energy Partners raised $10 billion in aggregate across three separate strategic funds, NGP recently closed a $3.25 billion fund, and Kayne Anderson is currently closing an oversubscribed energy fund. Carnelian Energy Capital and other players are also successfully generating private equity funds.

“It is kind of perfect timing for a financial sponsor to have fresh capital on the back end of this high-value, low-volume M&A and A&D cycle,” Hanson relates. “From a trend standpoint, typically what happens is that the post-M&A surviving company evaluates its pro forma portfolio of assets and determines which assets are non-core, and therefore, are not going to attract capital in its portfolio.”

Those same assets are often highly valuable to a private equity buyer or private equity portfolio company, Hanson goes on. “That will result in raising the A&D transaction volume back to the annual average. As a result, in 2025 and carried into the next several years, I fully expect that we will see a return to the average when it comes to transaction volume, including a high volume of middle-market A&D transactions.”

The biggest trend, Hanson believes, will be a reversion to more typical asset-focused A&D transactions with higher transaction volume, and a reversion to the annual average within the middle market.

“The re-emergence of a typically active A&D market is still in the early stages, but A&D activity is beginning to pick up in the United States, as evidenced by recent divestitures from companies such as APA Corp., Oxy, ExxonMobil, ConocoPhillips, and Chevron,” he reasons. “I believe this more active A&D market trend will continue to build in 2025, with further activity and the deployment of recently raised private equity capital in support.”

Based on historical trend cycles, Hanson suggests that the trend could last several years and will not be isolated to the lower 48. “This is really a global trend, as we are seeing opportunities now emerge in Africa, Southeast Asia, South America, and even Europe, in addition to the United States and Canada.”Hanson says there are many reasons to be optimistic about the upstream and midstream oil and gas sectors. “From an investor standpoint, there is a strong cash-on-cash return that is attracting capital back to the industry and given the current stakeholder return-focused mindset by management teams, I believe we will experience longevity. As the A&D trend reverts to the annual average, there is real reason for private equity investors to be encouraged about finding good opportunities to deploy capital and get meaningful returns, particularly over the next three to five years.”

Busy Period

Post Oak Energy Capital has typically closed one or two deals per year for more than a decade, but it ended with half a dozen in 2024, comprised of equity commitments and one divestiture.

“To be fair, a few of the deals that closed early in 2024 were mostly work that was done in 2023, but it has still been a busy period,” divulges Frost W. Cochran, founding partner and managing director. “There were two equity commitments in the Permian Basin, one each in the Utica and Haynesville shales, and significant investments in minerals.”

The lone divestiture was a produced water midstream entity. Given the growth of the produced water midstream services market, it may seem like a classic case of selling into strength, but Cochran says the goals for that investment were met, and it was moved to ownership where it could continue to grow.

“We are squarely in the distributions camp, returning a lot of cash to investors,” Cochran remarks. “With our new investments, we are drill bit-oriented. They are new assets that increase our presence in basins where we already have a presence. We still believe in core basins.”

For Post Oak Energy Capital, those basins include the Permian, Eagle Ford, Haynesville, Rockies, Mid-Continent, and some parts of Appalachia. “Clearly, you can underwrite to support demand growth again,” Cochran continues. “From 2023 onward, we have seen that LNG is real, and daily oil demand is strong again. Over the past two years, you have seen us putting companies back into business.”

Cochran stressed that the investment thesis is based on industry fundamentals and not politics. “Some people were holding off making any moves in an election year, but the fundamentals were screaming at us. Our heavy transactions occurred six to eight months before the election. Our thinking was that the outcomes of the elections did not really matter because we were going to need the gas regardless. The industry is not drilling to appease Washington—it is drilling to meet fundamental demand.”

Private equity always invests with the exit in mind first, and “the public companies are back,” Cochran states. “The mega deals last year got a lot of attention, and most recently, Marathon has been taken out, but there are still a lot of small operators in the Permian that will continue to be consolidated.” He points to Diamondback’s $3 billion acquisition of Double Eagle in February as a good example.

Post Oak also has a substantial position in mineral rights. “We have always bought minerals in the basins where we invest in operators,” Cochran explains. “It is a little different from the way others do business. We keep the minerals and hardly ever sell, even if we sell the operator, and sweep the proceeds into our distribution.”

That strategy keeps investors coming back for more. “We acquired $500 million in minerals last year—our highest year ever for that,” Cochran points out. “Our limited partners have asked for more exposure to that. They love it. They love the distribution.”

But Cochran admits that is not always the case. “We really had to sell our dry gas thesis pretty hard,” Cochran relates. “Twelve months ago, it was not obvious that was the smart move. Now the 12-month strip has touched $5 an Mcf, so you might not believe that dry gas was a hard sell. It is not just a weather phenomenon but a fundamental demand change. Similarly, it may not be comfortable to lean into oil demand today, but then 12 months ago it was not comfortable to lean into gas demand.”

Holding Discipline

Many companies are starting to move into refracs and other redevelopment opportunities in popular plays, observes Steve Kennedy, senior advisor at Opportune, a Houston-based energy consulting firm that also has an investment banking operation. “The Eagle Ford especially is seeing some of that. Producers are finding ways to extend their inventory rather than fighting it out to get into the Permian.”

Opportunities are even emerging offshore in the Gulf of America. “The Gulf has not received much interest in the last few years but has recently gained more attention. For instance, Texas Capital Securities facilitated a $350 million notes offering for W&T Offshore and Texas Capital Bank provided W&T with $50 million reserves-based lending. Prior to that, not many banks had been lending to offshore operations.”

Kennedy related a recent conversation in which a colleague referred to A&D in the Permian as two boxers slugging it out. “Many are choosing to step out and go to a different place rather than put the gloves on. A few are even falling back on conventional production. I have seen programs being put together by family offices, and some private equity firms are allocating some capital to conventional proven, developed, producing reserves.”

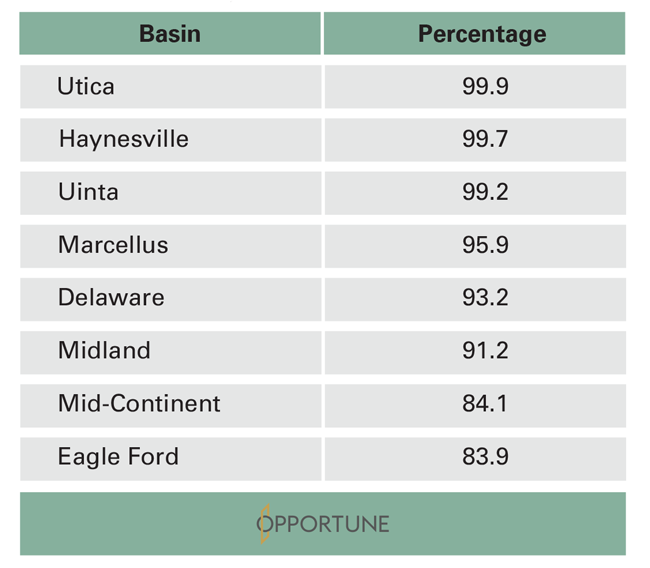

Another factor is the level of consolidation already achieved in many core basins. According to Opportune data, there has been almost a one-third reduction in the number of public operators in the United States, from 67 in 2019 to 46 today. The reduction among private operators has been even greater, dropping from 1,789 in 2019 to 753 today, a 42% decrease.

Along the same lines, the percentage of gross operated production controlled by the top 20 producers in most major basins has risen sharply. It is higher than 90% in six plays, and higher than 80% in two others (Table 1).

“There may be more capital available than can be usefully deployed all at once, but capital is not pouring into the sector so fast that it is causing problems in valuations,” Kennedy states. “Capital discipline is holding on both sides for both investors and operators.”

TABLE 1

Percentage of Gross Production

Controlled By Top 20 Producers (by Basin)

Source: Opportune

A&D multiples are an indicator. Opportune data show that of the 35 operated properties in the lower 48 sold in the 12 months prior to March 2025 for 3.4x earnings before interest, taxes, depreciation and amortization. On average, the deals were done at a price of $50,852 per daily flowing barrel of oil equivalent. While the trend is upward in both of those numbers, neither is outside the normal range. Gas deals were done at an average of $2,855 per daily flowing Mcf.

More broadly, public company valuations have risen, ranging from 3x EBITDA for BP to 7.5x EBITDA for EQT. “Two years ago, you were hard pressed to find anyone above 5x. The average at that time was 3.8x,” Kennedy recalls. “Today, the median is about 4.8x.”

Growing Organically

Amid all the transactions, it must be remembered that organic growth is still very much in the mix, ranging from recompletions and infill drilling to new export facilities.

In mid-February, Texas GulfLink–a greenfield deepwater crude export terminal–received its record of decision from the U.S. Department of Transportation’s Maritime Administration, approving its deepwater port license application. Sentinel Midstream, a portfolio company of Cresta Fund Management, is developing the terminal for very large crude carriers (VLCCs) 30 miles off Brazoria County, Tx.

“We looked at the existing infrastructure and realized that much of it was originally designed for a different era–one that did not anticipate today’s scale of crude exports,” says Wade Webber, managing director of Cresta and a director of Sentinel. “We believe there is a better, more efficient way to do things. That is not a criticism of existing facilities, just an acknowledgement that export markets and volumes have changed.”

The timeline for Texas GulfLink is dependent on further permitting, but once that is all in hand, actual construction is expected to take about two years. The design calls for loading at 85,000 barrels an hour, fast enough to fill a VLCC (cargo carrying capacity of ~2MM barrels) in a day.

Cresta has several other midstream portfolio companies, including a liquids system along the Gulf Coast, two joint ventures with ExxonMobil providing last-mile connections to their refineries, and a produced water operation.

“The water fundamentals in the Permian have really picked up in the past six to nine months,” Webber reports. “It used to be a reactive part of the value chain, but as water cuts and flowbacks have increased infrastructure planning has become much more coordinated. Water infrastructure is now a critical piece of upstream development.”

More broadly, he adds that “there are attractive investment opportunities in the private midstream sector that offer a healthy distribution yield and some insulation to commodity price volatility, relative to the upstream space. While midstream requires meaningful upfront capital, cash flows are typically contract-backed and stable—supporting higher conversion to distributions without the ongoing reinvestment demands of upstream.”

Cresta’s view of the midstream space is that the main themes across the industry will continue to create opportunities. “There is likely to be higher natural gas liquids production in the Permian as gassier benches get drilled, and those liquids are going to be hitting the Gulf Coast. That, along with higher crude exports and produced water midstream growth, is creating opportunities for capital investment.

“There are going to be even more opportunities for gas infrastructure as prices and production respond to demand pulls.”

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.