DUC Inventories Decline To Levels On Par With 2013

HOUSTON–According to Rystad Energy, the number of “live” drilled but uncompleted tight oil wells declined in June to the lowest level since 2013, a year in which WTI averaged $98 a barrel and the Permian Basin was producing only about 30% of its current daily oil volume.

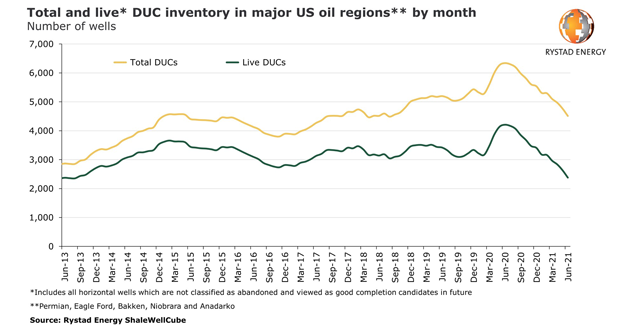

The total number of horizontal DUCs in the Permian, Eagle Ford, Bakken, Niobrara and Anadarko regions combined fell to 4,510 wells by the end of June. That implies a reduction of 1,800 wells from the peak of 6,340 in June 2020 and an average depletion of 150 wells a month over the prior 12 months. The last time the inventory was this small was in the second half of 2018, says Artem Abramov, head of shale research at Rystad Energy.

However, the total includes so-called “dead” DUCs, or wells that were drilled more than 24 months earlier and remain uncompleted, Abramov points out. “Empirical evidence shows that more than 95% of wells drilled are typically completed within the first two years, and hence the probability of those more than two years old getting completed now are low,” he says, noting that including dead DUCs to gauge future activity or forecast production is therefore often more speculative.

FIGURE 1

Monthly Total and ‘Live’ DUC Inventories in U.S. Tight Oil Basins

“Looking at the number of remaining live DUCs, a significant oil supply response from the U.S. onshore industry to the $70-$75/bbl WTI market is practically impossible before the first half of 2022,” Abramov observes. “Any further increases in fracturing, and subsequently well completions, will now require producers to first expand drilling by adding more rigs.”

Depleting DUCs

For months, operators have been depleting inventories of DUCs amid a slower drilling response in tight oil plays, with fewer active drilling rigs for each active frac spread. Consequently, live DUCs have declined across all major oil basins, with the Anadarko region the only exception. The depleting DUC inventory implies an increasing impetus on new well drilling to offset decline curves in tight oil basins.

In the Permian, only about 1,550 horizontal live DUCs remained at the end of June, representing a 37% (920-well) decline from the 2,470 wells in June 2021, according to Abramov. With Permian rig activity gradually becoming more robust–effectively doubling since bottoming out last fall–the total live DUC inventory count in the region is comparable to the second and third quarters of 2019.

“The picture across other major oil basins is more dramatic. South Texas’ Eagle Ford and the Bakken only have 300 live DUCs each left. Such a level in these two pioneering liquids plays has not been recorded since 2010,” says Abramov. “The inventory of live DUCs is down to 310 in the Niobrara region, which is the lowest since 2013.”

A breakdown of the total tight oil DUC inventory by spud vintage clearly shows that wells spud in 2019-20 had a significant weightage on fracturing activity as of June. While new wells are being drilled, the new inventory buildup in 2021 is insufficient to offset the depletion coming from pre-2021 vintage wells.

“In previous months, we repeatedly highlighted vintages from the fourth quarter of 2019 and the first three months of 2020 as key contributors of the unusually high DUC inventory buildup in the beginning of the COVID-induced downturn,” Abramov remarks. “By June 2021, 84% of those wells were completed. While it is still somewhat lower than the 14-month depletion rate of 92-93% recorded for Q4 2016-Q1 2017 and Q4 2017-Q1 2018 vintages, it is comparable to the 87% posted for the Q2 2018-Q1 2019 vintage between April 2019 and June 2020. Hence, this part of the DUC inventory anomaly has now been largely eliminated.”

While some degree of abnormality is still present, the industry is not that far off from a complete normalization of the DUC inventory level, he continues. The number of horizontal live DUCs per rig had already declined to 6.4 wells in the Permian and 9.2 in other major oil regions as of June 2021. Before the COVID-19 downturn, the level was at 3.9 for the Permian and 6.4 across other oil regions.

“Given the current activity and depletion trend, the industry will likely see a complete normalization by the end of September in the Permian, and by September-October across other oil regions,” Abramov concludes.

For other great articles about exploration, drilling, completions and production, subscribe to The American Oil & Gas Reporter and bookmark www.aogr.com.